Chiara Oppi

Investigating the role of accounting in

healthcare organizations:

Academic Year

2016/2017

PhD Course:

International Ph.D. in Management:

Innovation, Sustainability and Healthcare

Investigating the role of accounting in

healthcare organizations:

traditional costing and new approaches

Author

Chiara Oppi

Supervisor

Professor, Dr. Lino Cinquini

Institute of Management

Sant’Anna School of Advanced Studies

Pisa, Italy

Tutor

Professor, Dr. Emidia Vagnoni

Department of Economics and Management

University of Ferrara, Italy

1

Table of Contents

Executive summary ... 5

Chapter 1 ... 9

Introduction to the thesis ... 9

1. Motivation ... 9

2. The research questions ... 13

3. Steps of the research, method and data collection ... 18

3.1 The Accounting Information Systems ... 18

3.2 Steps of the research ... 19

3.2.1 Step 1: Literature review ... 20

3.2.2 Step 2: Case study ... 20

3.2.3 Step 3: Survey ... 21

4. Findings ... 22

4.1 Results from the literature review ... 23

4.2 Results from case study ... 25

4.3 Results from the survey ... 26

5. Contributions of the thesis, limitations and direction for future research ... 28

5.1 Which factors can foster clinicians’ resistance to AISs or can increase clinicians’ use of AISs in HCOs? ... 28

5.2 Do clinicians and controllers collaborate in the design of AISs that take into account both groups’ information needs for decision making?... 29

5.3 Do clinicians perceive AISs adaptable to the care activity they perform? ... 30

5.4 Does the structural configuration influence clinicians’ perception of AISs adaptability? Does medical specialty influence clinicians’ perception of AISs adaptability? ... 31

5.5 Contribution ... 31 6. References ... 34 Chapter 2 ... 44 Abstract ... 44 1. Introduction ... 45 2. Method ... 47

2.1 Refining the question ... 47

2.2 Inclusion/exclusion criteria... 48

2.3 Literature search ... 48

2.4 Screening the results and assessing the quality of the selected articles ... 49

2.5 Synthesizing the findings ... 49

2.6 Analysis of results ... 49

3. Presentation of descriptive data ... 50

2

3.2 Research settings ... 53

3.3 Research methods deployed ... 53

4. Discussion of findings ... 54

4.1 Clinicians’ education and training ... 55

4.2 Collaboration between controllers and clinicians and power of the two groups ... 56

4.3 Characteristics of AISs ... 59

5. Emerging directions for future research ... 63

6. Conclusions ... 64 7. References ... 66 8. Appendices ... 76 Chapter 3 ... 79 Abstract ... 79 1. Introduction ... 80 2. Literature review... 82

2.1 The changing role of controllers in healthcare ... 82

2.2 The identity work framework ... 83

2.3 Controllers’ identity work in healthcare ... 85

3. Methodology ... 86

4. Results and discussion ... 88

4.1 AISs: the status quo ... 89

4.2 Controllers’ identity work: coercive control and autonomy ... 90

4.3 Provision of information to clinician mangers ... 95

5. Conclusions ... 98 6. References ... 100 Chapter 4 ... 106 Abstract ... 106 1. Introduction ... 107 2. Research setting ... 109 3. Literature review... 111

3.1 Accountability structures and perceived AISs adaptation ... 111

3.2. Medical education and perceived AISs adaptation ... 112

4. Design of the study ... 115

4.1 Exploratory interviews ... 115

4.2 Survey sample ... 116

4.3 Measurement of variables ... 116

4.3.1 Dependent variable: perceived AISs adaptability ... 116

4.3.2 Independent variable 1: type of structure ... 118

3

5. Results ... 118

5.1 Research question 1 – Do perceptions of AISs adaptability differ between the two structural configurations? ... 118

5.2 Research question 2: Does type of specialization matter to perceptions of AISs adaptability? 120 5.3 Additional analysis ... 123

6. Discussion of results... 124

7. Limitations and concluding comments ... 128

8. References ... 129

4

List of Tables

Table 2.1: Characteristics of articles for data collection………... 49

Table 2.2: Distribution of the selected articles across the types of journal………... 51

Table 2.3: Synthesis of organizational factors and main findings……… 61

Table 3.1: Common themes emerging from interviews and summary of findings………... 89

Table 4.1: Descriptive statistics for perceived AISs adaptability………...117

Table 4.2: Analysis of variance (type of structure)………..119

Table 4.3: Analysis of variance (type of structure, single-items considered)………..119

Table 4.4: Analysis of variance of the 3-item perceived adaptability constructs and structural configuration………...120

Table 4.5a: Analysis of variance among specialization and perceived AISs adaptability………....……...121

Table 4.5b: Analysis of variance between the different specializations………..121

Table 4.6: Analysis of variance on 6-item perceived adaptability construct and two groups of specializations (general surgery and combined internal medicine and radiology) –ANOVA…… ……….122

Table 4.7: Analysis of variance between the 3-item perceived adaptability construct and the two specializations (i.e. general surgery and combined internal medicine and radiology)……….122

Table 4.8a: Descriptive statistics and two-way analysis of variance (type of structure * general surgery and combined internal medicine and radiology)……….123

Table 4.8b: Tests of Between-Subjects Effects………...124

List of Figures

Figure 1.1: Summary of research questions and methods adopted………...19Figure 2.1: Trend of publication of articles over time in total and narrowing the field of investigation……….. ..51

Appendices

Appendix 2.1: List of journals considered in the review process (according to Chartered Association of Business Schools’ Academic Journal Guide 2015)………... 76Appendix 2.2: Distribution of the selected articles across the journals……… 78

5

Executive summary

This dissertation contributes to the literature concerning clinicians’ approach toward accounting information systems (AISs) in healthcare organizations (HCOs) and clinicians’ needs in AISs implementation.

AISs have gained increasing relevance in healthcare since organizations have been required to provide data that support planning, monitoring and reporting, with the aims to both allow benchmarking and assessing organizational and individual performance. In this process, clinicians have been also attributed the role of mangers. They have become the recipients of accounting information, thus the provision of data directed at increasing their cost-consciousness in decision making has become a challenge.

Since literature shows the clinicians’ negative approach regarding their managerial roles, a broad body of research has deepened the factors hindering their full involvement in management and incentivizing their resistance toward accounting. This body of literature claimed for an investigation of the causes that, three decades after the enhancement of managerial reforms, still hinder clinicians’ full involvement in management and prevent them from using AISs in healthcare organizations. In fact, whether literature deepened both contextual and organizational factors affecting clinicians’ resistance to AISs, space for action remains with reference to the exploration of this issue at organizational level.

The current research aims at deepening this issue. Following literature’s call, the research adopts a narrow focus on the organizational factors and answers the following main research question: Which factors can foster clinicians’ resistance to accounting information systems or can increase clinicians’ use of AISs in healthcare organizations?

To this aim, this dissertation first analyses the literature in the field to identify the most relevant themes emerging and the topics requiring further investigation.

Second, the dissertation explores, by empirical analysis, the main factors that appear to affect clinicians’ resistance to accounting in healthcare: (a) the patterns of collaboration between clinicians and controllers in the design of AISs; (b) clinicians’ perception of AISs adaptability to their information needs, according to the type of organization in which clinicians work and their medical education.

The dissertation is divided into three parts, which contribute theoretically and empirically to answer the main research question.

The first step consists of a systematic literature review that explores the high-quality accounting, management, and social sciences literature with the aim to identify the main issues related to clinicians’ resistance to AISs in HCOs and the organizational factors that exacerbate or hinder

6

clinicians’ involvement in management. To this trail, the review examines 79 papers and allows at detecting the topics investigated and the trend of publication over time, and to identify the main factors that affect clinicians’ approach to accounting and require further investigation. Three main streams of research emerged: (i) relationships between clinicians and controllers, (ii) the characteristics of AISs that may increase clinicians’ involvement in management, and (iii) medical education. The review’s findings result in a series of hints for the development of the empirical stages of the research, which are conducted investigating the Italian setting, and adopting both qualitative and quantitative approaches. The following steps deepen the above three factors by empirical investigation.

The second step of this dissertation consists in a case study conducted in a single organization and directed at investigating whether clinicians and controllers collaborate in the design of AISs. Interviews with both controllers and clinicians reveal that the coercive control coming from regulations has challenged controllers’ autonomy and changed their role in the organization. In this sense, controllers appear to be less focused on performing an actual management control and more committed to the design of AISs that satisfy normative requirements, while they fail in providing clinicians with valuable accounting information for decision-making. It emerges that the characteristics of AISs implemented in HCOs differ from those who may increase clinicians’ managerial approach.

The third step of the research presents a survey directed at assessing clinicians’ perception of accounting systems’ adaptability to their needs. The research, in particular, explores the impact of two factors on clinicians’ perceptions of AISs adaptability: HCOs structural configuration, in terms of decentralization of decisional processes and involvement of clinicians in the design of AISs that fit their needs, and clinicians’ medical education. The survey has been conducted among 304 clinicians working in Local Health Authorities and independent hospital in six Italian regions. Results show that the differences between the two structural configurations are not significant. However, when AISs capability to adapt to more patient-focused approaches is considered, AISs in independent hospitals are perceived more adaptable. It emerges that independent hospitals’ characteristics allow at involving more clinicians in decision making and at designing AISs that are more consistent with clinicians’ needs. In addition, the survey provides evidence of the differences between surgeons and other clinicians, and of surgeons’ lower perception of AISs adaptability. This supports the idea of the existence of a surgeon stereotype that influences clinicians’ accounting choices and their willingness to be involved in management.

The three steps allow at answering the main research question, extending the knowledge in accounting literature of the factors that affect clinicians’ approach to accounting in healthcare

7

organizations. The research address literature’s call for an investigation of the organizational factors that hinder clinicians’ involvement in management. The study identifies the factors that worth further research in this sense, and then empirically deepens these factors. It contributes to increase accounting’s knowledge about the patterns of collaboration between clinicians and controllers, the characteristics of AISs that increase clinicians’ involvement in management and the effect of medical education on clinicians’ approach to accounting. In this sense, the study contributes to accounting literature using both qualitative and quantitative methods, and highlights the inadequacy of existing AISs and the scarce involvement of clinicians in the design of AISs, as a consequences of strict regulations and the centralization of decision making processes. Furthermore, it explores the impact of structural configurations and medical education on clinicians’ perception of AISs adaptability to the changes occurring in HCOs.

Future researches could investigate the relevance of the themes emerging in this research in other contexts with different characteristics. Research is also needed to deepen how medical education can increase clinicians’ willingness to assume managerial roles, and how organizations can push clinicians toward accounting, while decentralizing decisional processes and incentivising controllers to involve clinicians in AISs design.

9

Chapter 1

Introduction to the thesis

1. Motivation

In the healthcare context, the role of accounting information systems (AISs) is of great interest to analyse the potential of accounting discipline to contribute to increase efficiency (Marcon and Panozzo, 1998). Healthcare organizations (HCOs), in fact, are experiencing economic concerns related to the increasing costs of the health services provided and, as a consequence, their economic sustainability is often questioned (Negrini et al., 2004; Lehtonen, 2007).

During the last three decades, in fact, since HCOs worldwide have undergone through a series of managerial reforms under the label of “New Public Management”, the healthcare sector has been subject to managerial changes that put emphasis on economic results, introduce managerial tools, and new AISs (Marcon and Panozzo, 1998; Adinolfi, 2014; Macinati and Anessi-Pessina, 2014). Those reforms proposed a managerial approach centred on planning and budgeting with the aim to improve both the services’ quality and the production process’ efficiency. Therefore, HCOs introduced AISs and other managerial tools to bridge the new requirements coming from managerial reforms, which enhance cost-containment policies, and the fulfilment of clinical objectives (Marcon and Panozzo, 1998; Adinolfi, 2014).

In particular, HCOs were required to support the process of change by designing AISs that could pursue cost-containment objectives while allowing benchmarking between healthcare organizations in the same setting (Llewellyn and Northcott, 2005; Lehtonen, 2007; Guven Uslu and Conrad, 2008; Järvinen, 2009).

In that dynamic era, clinicians have gained a new role; they became responsible for the achievement of specific economic and quality objectives, and their clinical practice evaluated (Jacobs, 1995, Nyland and Pettersen, 2004; Scarparo, 2006). In this sense, due to clinicians’ great impact on costs (Abernethy and Stoelwinder, 1995), the role of clinician managers was introduced (Llewellyn, 2001) to increase their commitment to cost-containment policies and incentivize their acceptance of the managerial role.

In this context, the increasing involvement of clinicians in managerial activities required the provision of administrative support to them, in terms of management reports of performance measures related to a strict budget approach (Lapsley, 2001). Thus, AISs have been directed at increasing clinicians’ cost-consciousness in their decisional processes (Coombs, 1987) and have

10

been required to satisfy both internal and external needs, combining financial data with information more related to the care activity performed.

The integration of financial information with non-financial data allowed to address the needs of the different actors involved in internal management, to increase the sphere of performance measurement (e.g. information on quality, flexibility, outcomes…), while linking data to resource utilization for accountability purposes (Ballantine, 1998). This led one side to the adoption of management control systems, and consequently to the provision of management accounting information centred on budgeting; on the other side to accountability processes directed at showing the link of budget decisions with HCOs’ activity and financial planning (Marcon and Panozzo, 1998).

In this sense, AISs has included, among the others: financial accounting systems, costing systems (cost center costing, activity-based costing), patient costing, performance data, and reports on budgets’ goals achievement (Coombs, 1987). Further, AISs combined the provision of data with both short-term and long-term focus (Ballantine, 1998).

Since the enactment of managerial reforms and the revision of AISs following the involvement of clinicians in management, literature has focused on clinicians’ approach to AISs. Literature investigated the role of clinicians and their attitude towards the use and acceptance of AISs (Bosa, 2010; Coombs, 1987; Abernethy and Vagnoni, 2004), as clinicians mainly showed resistance towards accounting (Llewellyn, 1998; Kurunmäki, 1999; 2004; Burns and Scapens, 2001; Abernethy and Vagnoni, 2004; Lehtonen, 2007). Among the studies that have considered the influence of clinicians on AISs, many of them suggest to further investigate the role of clinicians as managers. In particular, literature advocates for an investigation of the causes that three decades after the enhancement of managerial reforms still hinder clinicians’ full involvement in management and prevent them from using AISs in decision making (Fulop, 2012; Börner and Verstegen, 2013; Kastberg and Siverbo, 2016). Among those, literature focused on the factors at both contextual and organizational levels, calling for a further investigation of the actions to be implemented to overcome clinicians’ resistances to AISs and incentivise their managerial attitude (Kippist and Fitzgerald, 2009; Börner and Verstegen, 2013; Campanale and Cinquini, 2016). The literature investigating contextual factors calls for the involvement of clinicians in the public debate with policy makers (Baker and Denis, 2011; Malmmose, 2014).

The literature investigating organizational level advocates for the reinforcement of the collaboration between clinicians and controllers to strengthen clinicians’ commitment to accounting, while ensuring their power (Lehtonen, 2007; Macinati, 2010; Baker and Denis, 2011; Börner and Verstegen, 2013). Considering the important role of controllers in designing AISs in HCOs, further

11

research is also required to gain a better understanding of the difficulties experienced by clinicians and controllers in cooperation (Naranjo-Gil et al., 2009; Kantola, 2015; Fiondella et al., 2016). Furthermore, the medical educational path strengthens clinicians’ autonomy and prevent them from being involved in management (Jacobs, 2005; Torbica and Fattore, 2010), thus this is a further research area to develop (Fiondella et al., 2016; Kastberg and Siverbo, 2016).

In addition, the literature has investigated the new information needs emerging from innovative diagnoses and treatments, transversal processes and organizational changes, and has highlighted the inadequacy of traditional cost center accounting tools (Vera and Kuntz, 2007; Demeere et al., 2009). In fact, traditional tools do not support clinicians in managing the emerging costs coming from innovation, facing budget constraints and undertaking activities directed to cost reduction (Ernst and Szczesny, 2008). Thus, the need to further explore how AISs should be designed to address clinicians’ needs and provide a stricter link between costs and resource utilization emerges (Vera and Kuntz, 2007; Eldenburg, 2010; Campanale et al., 2014; Macinati and Rizzo, 2014). The aim of this dissertation falls in the research arena of clinicians’ approach toward AISs in HCOs and clinicians’ needs in AISs implementation. Thus, the purpose of the dissertation is multiple. First, based on the lack of literature reviews focusing on the factors within HCOs that affect clinicians’ resistance to AISs, the research aims at synthetizing and analysing the broad literature in the field, contributing at identifying the most relevant themes emerging and the topics requiring further investigation. Second, the research aims at contributing to the literature addressing the main streams of research identified in the review, namely the patterns of collaboration between clinicians and controllers, AISs adaptability to clinicians’ information needs, and medical education. In particular, the research is directed at increasing accounting literature consciousness about controllers’ role in HCOs in the design of AISs that satisfy both controllers and clinicians needs. Furthermore, the research addresses the call emerging from the literature related to a deeper analysis of AISs capability to adapt to changes occurring in HCOs and the impact medical education plays in clinicians’ involvement in management.

Thus, this research aims to: (i) identify the main issues related to clinicians’ resistance to AISs in HCOs and the main factors that can enhance their commitment to assume managerial roles; (ii) explore the patterns of collaboration of clinicians and controllers in HCOs; (iii) investigate if and how AISs balance both clinicians’ information needs for decision making and controllers’ attitude in the design and implementation of AISs; and (iv) investigate the factors that can enhance clinicians’ perception of AISs adaptability to their needs and to the care activity performed.

12

The first contribution of this thesis lies in the narrow focus on the factors that affect clinicians’ resistance toward AISs at organizational level. Conversely to previous literature reviews in the field (Cardinaels and Soderstrom, 2013; Abernethy et al., 2006; Raulinajtys-Grzybek 2014), which mainly addressed the topic focusing on the effects of external factors such as institutional changes, the review contributes to accounting literature shedding light on the impact of organizational factors on clinicians’ resistance to AISs, and then identifying the major themes to be considered for future researches. The systematic literature review allows to (i) identify how literature addressed this issue, in terms of trend of publication over time, context and methodology, (ii) show which factors within HCOs have been found by literature to impact on clinicians’ resistance to AISs, and (iii) identify the main research areas for future investigations.

Findings of this literature review highlight the need to investigate (i) the effect of medical education on clinicians’ approach to accounting; (ii) the processes of collaboration between clinicians and controllers in HCOs and (iii) the specific characteristics of AISs which may increase clinicians’ willingness to assume managerial roles and their use accounting information for decision making. In this sense, the research shows that is still needed a contribution to root accounting in clinicians’ decisional processes. Considering gaps and future researches suggested by the literature review, this thesis aims to contribute to filling the gaps, and providing additional contributions through empirical investigation.

The second contribution of this thesis concerns the exploration, through empirical analysis, of the relationship between clinicians and controllers in the design of AISs, on the light of the increasing relevance of controllers in HCOs. The study highlights that the main driver of AISs design comes from the government that searches for AISs that allow comparability and benchmarking among organizations, rather than AISs providing clinician with information for internal decision making. As a result of this government control over AISs, controllers have scarce possibilities to affect AISs to take into account clinicians’ information needs. The research shows that regulations and normative requirements have limited the autonomy of controllers, thus reducing the possibilities to design AISs with the contribution of clinicians. Clinicians claim for AISs that are more process-based rather than cost centre-process-based, as required by regulations, and ask for an increasing involvement in the design of AISs, while controllers acknowledge the need for this change. However, controllers report that the strict normative control has increased the emphasis on accountability over time, while limiting their capability to address clinicians’ needs in the design of AISs and to change the current design of AISs through the involvement of clinicians. Although controllers recognize the scarce usefulness of AISs for internal decision making, their low capability to influence the implementation of AISs reduces the possibility to collaborate with

13

clinicians, and increases clinicians’ resistance to the use of AISs. Thus, the study contributes to literature about the patterns of collaboration between clinicians and controllers in the design of AISs, emphasizing the loss of decisional power of controllers in the organization and their subjugation to regulations, which has consequences on the scarce capability to involve clinicians and to address their information needs in AISs’ design.

The third contribution of this thesis relies on the investigation of the scarce capability of AISs to adapt to clinicians’ needs and of the factors that affect clinicians’ perception of AISs adaptability. Accounting literature has stressed the importance of understanding whether AISs are designed according to organizational changes and care activity, and the consequences on clinicians’ AISs adaptability to their needs (Smith et al., 2005; Börner and Verstegen, 2013; Pettersen, 2013). In particular, following accounting literature, two mayor factors influencing clinicians’ perception have been identified: HCOs’ structural configuration, in terms of decentralization of decisional processes in the organization, and medical education.

Structural configuration has been scarcely investigated in healthcare, while accounting literature found that it affects users’ perception of AISs adaptability to their needs (Abernethy and Bowens, 2005). On the other side, medical education has been found to affect clinicians’ personal characteristics, and further research is required concerning its impact on clinicians’ involvement in accounting (Torbica and Fattore, 2010; Kastberg and Siverbo, 2016).

In this sense, through a quantitative approach, the study contributes to literature investigating the impact of those factors on clinicians’ perception of AISs adaptability to the care activity performed in HCOs. More in depth, through a survey conducted in different organizations, the research shows that also in healthcare the centralization of decision processes is likely to reduce clinicians’ perception of AISs adaptability. Furthermore, the study provides evidence of the impact of different medical specialities on clinicians’ approach to AISs, and in particular on surgeons’ higher resistances to assume managerial roles.

This chapter is organized as follows: next section describes the research questions that drive the research process, while section 3 explains the methodology applied. Further, the following section provides a summary of the findings, while the fifth section explains the theoretical and practical contributions of the study, reports the limitations and outlines future research directions.

2. The research questions

Literature has widely investigated the patterns of implementation of AISs to address the requirements coming from managerial reforms, and the willingness of clinicians to assume

14

managerial roles (Kurunmaki et al., 2003; Nyland and Pettersen, 2004; Lapsley, 2007; Börner and Verstegen, 2013).

More in depth, literature reported clinicians’ long lasting resistance toward AISs (Pfeffer, 1992; Abernethy and Stoelwinder, 1995; Arai, 2006), which has had negative effects on the capability of HCOs to implement effectively AISs and to pursue managerial reforms’ aims (Jacobs, 1995; Jones and Dewing, 1997; Nyland and Pettersen, 2004; Lapsley, 2007). Still, after more than three decades, clinicians have resisted and have not integrated AISs in their activities (Adinolfi, 2014; Gebreiter, 2016; Wickramasinghe, 2015; Fiondella, 2016).

This resistance suggests the existence of factors within HCOs hindering clinicians’ acceptance of AISs. In fact, HCOs have failed over time in pushing clinicians’ behaviour toward the assumption of managerial responsibilities (Coombs, 1987; Harrison et al. 1989; Kurunmaki, 1999; Jones, 2002; Forbes et al., 2004). This enduring resistance suggests that there may be organizational factors that exacerbate clinicians’ negative approach to AISs, and that there is space for action in accounting for research about methods to overcome those resistances.

Despite the extensive literature in the field, few researches aimed at providing a comprehensive view of the factors that affect clinicians’ approach to AISs in HCOs. Literature reviews have deepened the theme with reference to the institutional changes and their consequences on AISs (Cardinaels and Soderstrom, 2013; Abernethy et al., 2006), or focused on the specific role of different AISs (Raulinajtys-Grzybek 2014). Reviews mainly centred on the impact of factors emerging at institutional level and little attention has been paid to reviewing the influence of organizational factors on clinicians’ resistance. Given this gap in the literature, the need to provide a comprehensive overview of the organizational factors that affect clinicians’ resistance to AISs emerges. To this aim, a first general research question was framed:

RQ1: Which factors can foster clinicians’ resistance to AISs or can increase clinicians’ use of AISs in HCOs?

Given the complexity of the topic, this dissertation aims at answering the general research question identifying in the literature the main factors influencing clinicians’ approach to AISs in HCOs and deepening those factors through empirical investigation. To this aim, the research addresses the research questions presented in the following paragraphs, aiming at providing a comprehensive view of the determinants of clinicians’ approach. Thus, the general research question stated is addressed through the cumulative investigation of the following streams of research.

One of the factors affecting clinicians’ approach to AISs in HCOs refers to clinicians’ capability to interact with controllers. In fact, healthcare shows a dichotomy between clinical and managerial

15

issues, in terms of a separation between clinicians’ focus on care delivery and controllers’ role in administrative activities (Mintzberg, 1983). Although clinicians had traditionally a dominant role in HCOs, managerial reforms emphasized the shift in power from clinicians to controllers (Jones, 2002) and strengthened the role of controllers in the implementation of AISs (Naranjo-Gil et al., 2009; Kantola, 2009).

Controllers are the first recipient of managerial innovation and are those who design AISs, so they have a relevant power in influencing AISs (Bourn and Ezzamel 1986; Purdy and Gago, 2003; Järvinen, 2009; Naranjo-Gil et al., 2009; Macinati and Anessi-Pessina, 2014; Kantola, 2015). Controllers are required to adapt AISs to the requirements coming from managerial reforms and cost-containment policies that strengthened the control over HCOs’ activities, while also addressing the information needs of other actors in HCOs, clinicians in particular (Tediosi et al., 2009; Vagnoni and Maran, 2013; Fiondella et al., 2016). Following the normative requirements, HCOs have been pushed toward the implementation of AISs that allow benchmarking and comparability (Guven Uslu and Conrad, 2011; Fiondella et al., 2016). This increased importance of controllers in the design of AISs, and reduced clinicians’ capabilities to push a change in accounting (Jones, 2002), with the consequence that clinicians do not perceive AISs consistent with needs and resist the change (Szczesny and Ernst, 2016).

Therefore, literature showed the importance of investigating how the relationships between clinicians and controllers in the design of AISs can facilitate or hinder the implementation of AISs that address clinicians’ needs (Østergren, 2009; Fiondella et al., 2016). However, some issues still require further investigation. In particular, on the light of the role controllers exert and the growing focus on benchmarking and comparability, literature has called for an exploration of power mechanism in HCOs in the design of AISs (Østergren, 2009). In addition, literature has required deepening the capability of clinicians to be involved in the design of AISs and to revise them according to their needs (Kraus et al., 2016).

Given the increased importance of the role of controllers in HCOs and the gaps identified in the literature, space for action emerges with reference to the exploration of the patterns of collaboration between clinicians and controllers in AISs design, on the light of the regulations that increased controllers’ role in HCOs and reduced clinicians’ power.

Therefore, the second research question is:

RQ2: Do clinicians and controllers collaborate in the design of AISs that take into account both groups’ information needs for decision making?

16

Another factor affecting clinicians’ resistance to accounting refers to the characteristics of AISs and to the type of information provided.

Clinicians’ involvement in the design of AISs can increase their perception of AISs’ adaptability to their information needs, in terms of alignment to the care activity performed and to the changes that took places in HCOs (Lachman et al., 2013). On the contrary, clinicians’ resistance emerges when cost center AISs are effective to support the well-established professional bureaucratic model (Mintzberg, 1992), and lack in focusing on the organizational processes, being designed to allocate costs to accountability units and cost centers (Cannavacciulo et al., 2015). In fact, cost center AISs do not provide detailed and clinical-oriented cost information (Campanale et al., 2014; Negrini et al., 2004) and increase clinicians’ resistance to use AISs for decision making.

The AISs that have been implemented in HCOs following the reforms are missing to support clinicians’ decision making processes and to enhance a managerial approach that takes into account resources constrains, being also clinical oriented (Campanale et al., 2014). In this sense, accounting systems no longer seem to be adequate to the healthcare setting (Negrini et al., 2004) as organizational changes and innovative treatments have not been accompanied by a change in AISs that allowed efficient cost consumption (Gebreiter and Ferry, 2016).

On the contrary, when AISs are centred on clinicians’ needs, they may help in enhancing effective operational and strategic decision making processes, which are based on the new organizational needs (Chan, 1993; Hoyt and Lay, 1995). Thus, literature emphasizes the importance to explore the extent to what AISs are designed to fit organizational changes and changes in care activity (Börner and Verstegen, 2013). In addition, literature calls for an investigation of the differences in AISs among HCOs, to detect whether a change in accounting has occurred following organizational and care activity changes and to assess if AISs have the capability to increase clinicians’ willingness to assume managerial roles (Smith et al., 2005; Pettersen, 2013).

To this extent, the relevance of investigating whether clinicians perceive AISs adaptable to the activity performed in HCOs and to their needs emerges. Thus, the third research question is:

RQ3: Do clinicians perceive AISs adaptable to the care activity they perform?

To address this research question is required a deeper investigation of the determinants of clinicians’ perception of AISs adaptability to the care activity performed. In this sense, based on literature, clinicians’ perception of AISs adaptability is influenced by factors that refer to both the structural configuration of the organization, in terms of information asymmetries and involvement in decisional processes (Abernethy, Bouwens and van Lent, 2004; Pizzini, 2010), and the medical education received, in terms of specialty (Forbes et al., 2004; Jacobs, 2005; Torbica and Fattore,

17

2010). For this reason, to answer the above cited research question, both structural configuration and medical education will be investigated.

Clinicians’ perception of AISs adaptability depends on the extent to what AISs address their information needs, thus it relies on the involvement of clinicians in the design of AISs. In this sense, HCOs’ decentralization of decisional making processes and information asymmetries can influence clinicians’ perception of AISs adaptability. In fact, the accountability structures and the information asymmetries emerging when decision making processes are implemented strongly affect the way in which actors perceive AISs to be adaptable to their needs (Abernethy, Bouwens and van Lent, 2004; Gerdin, 2005; Hansen, 2010).

In HCOs, clinicians perceive AISs to adapt to their needs if they are involved in decisional processes related to the design of AISs (Pizzini, 2010). In this sense, the structural configuration of HCOs, in terms of centralization or decentralization of decisional processes, can play a role in enhancing or reducing clinicians’ resistance. More in depth, whether centralization of decision processes increase resistance toward changes in AISs, because AISs may not fit users’ information needs, decentralization and the involvement of actors in decision making is a way of overcoming this issue (Abernethy and Bouwens, 2005). In fact, decentralization of decisional processes allows a broad involvement of different actors in the design of AISs and increases accounting capability to adapt to changes (Chenhall, 2005; Malina and Selto, 2004).

However, there is little research focusing on AISs adaptability and its determinants in healthcare, in particular with reference to the effects of structural configuration on clinicians’ resistance to AISs. In this sense, the importance of investigating the consequences of different structural configurations among HCOs emerges. This generates an additional research question:

RQ4: Does the structural configuration influence clinicians’ perception of AISs adaptability? Clinicians’ understanding of managerial issues, their education, and their personal characteristics also influence clinicians’ information needs and their willingness to assume managerial roles. In particular, medical education plays a role in reducing clinicians’ resistance to AISs and, more in general, in pushing their commitment toward accounting (Forbes et al., 2004; Jacobs, 2005; Torbica and Fattore, 2010). In this sense, although managerial training has the power to cope with clinicians’ resistance (Jacobs, 1995; Carlström, 2012; Macinati and Rizzo, 2014), medical specialty should be taken particularly into account, as it has been found to influence clinicians’ personal characteristics and attitudes in HCOs (Coombs et al., 1993; Borges and Osmon, 2001; Chan and Ahmad, 2011). Although extensive research has investigated the consequences of medical education on clinicians’ behaviours, literature has not deepened the effects of medical education on

18

clinicians’ approach to AISs. In this sense, accounting literature has claimed for an investigation of clinicians’ professional identity and of their medical education (Kastberg and Siverbo, 2016), and their consequences on management, with the aim to implement different strategies to increase clinicians’ willingness to assume managerial roles (Macinati and Rizzo, 2014). Thus, the effects of clinicians’ education and their medical speciality on clinicians’ perception of AISs adaptability require further exploration (Torbica and Fattore, 2010; Kastberg and Siverbo, 2016). From this, the fifth research question emerges:

RQ5: Does medical specialty influence clinicians’ perception of AISs adaptability?

3. Steps of the research, method and data collection

3.1 The Accounting Information Systems

Healthcare organizations perform a series of activities that require the provision of data to support planning, monitoring and reporting functions. Given their publicly financed nature and the complexity of HCOs, in many contexts, and in the Italian one, the design of detailed information is necessary to both allow public accountability (Lawrence et al., 1997) and to provide information for management, planning and control that enables conscious decision making in the organization (Lawrence et al., 1994; Burns and Scapens, 2000). Moreover, the increased autonomy of healthcare organizations and the involvement of clinicians in managerial activities has moved accounting systems from the sole focus on financial data toward the provision of non-financial information concerning organizational and individual performance (Marcon and Panozzo, 1998).

In the last three decades, although AISs have come over time to constitute stable routines (Burns and Scapens, 2000; Macinati, 2010) in HCOs, which have increased their sophistication over time (Smith et al., 2005), AISs have been continuously revised.

In the last decade in particular, HCOs in many contexts, and in the Italian healthcare sector object of study, have faced a new trend of increasing accountability duties related to cost-constraints and the need to account for cost efficiency and allow comparability (Järvinen, 2009; Fiondella, 2016). Thus, the pool of accounting instruments implemented has grown over time based on the requests coming from national and local governments (Fiondella et al., 2016). For this, Italian HCOs nowadays face the need to combine the existing AISs with additional reports required by local and national regulatory frameworks, which are mainly directed at enhancing benchmarking among organizations (Järvinen, 2009; Fiondella et al., 2016).

19

3.2 Steps of the research

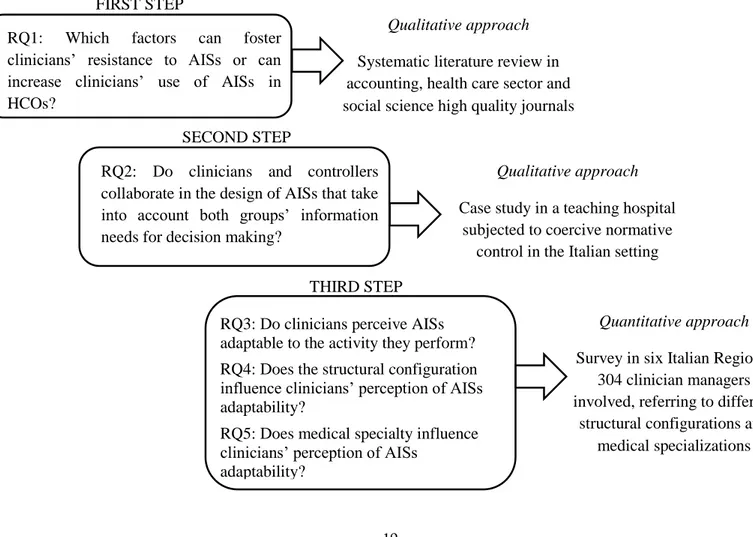

This thesis has been developed by the application of multiple methods in the different steps. The different approaches adopted have been considered suitable to address the research questions described in section 2. In this sense, both qualitative and quantitative methods have been adopted. Qualitative methods refer to a systematic literature review and a case study. One side, the literature review allowed at addressing research question n.1, providing a broad view of the relevant literature in the field of study, and exploring the factors affecting clinicians’ resistance to AISs. On the other side, through the case study approach, the research deepened the patterns of cooperation between clinicians and controllers, and controllers’ perception of their role in the organization, answering research question n.2. Quantitative methods, conversely, allowed exploring more widely the factors that contribute to increase or reduce clinicians’ perception of AISs adaptability to the care activity performed and the changes occurring in HCOs. Consistent to this, a survey approach allowed at comparing different settings, organizations and type of professionals, addressing research questions n. 3, 4, 5.

Figure I summarizes the three steps of the research process, the research questions addressed and the methods applied.

Figure 1.1: Summary of research questions and methods adopted

RQ1: Which factors can foster clinicians’ resistance to AISs or can increase clinicians’ use of AISs in HCOs?

Qualitative approach

Systematic literature review in accounting, health care sector and social science high quality journals

RQ2: Do clinicians and controllers collaborate in the design of AISs that take into account both groups’ information needs for decision making?

Qualitative approach

Case study in a teaching hospital subjected to coercive normative

control in the Italian setting

RQ3: Do clinicians perceive AISs adaptable to the activity they perform? RQ4: Does the structural configuration influence clinicians’ perception of AISs adaptability?

RQ5: Does medical specialty influence clinicians’ perception of AISs

adaptability?

Quantitative approach

Survey in six Italian Regions, 304 clinician managers involved, referring to different

structural configurations and medical specializations FIRST STEP

SECOND STEP

20

3.2.1 Step 1: Literature review

The first step of the research concerns a systematic literature review aiming at understanding the main factors that can exert clinicians’ resistance to AISs in HCOs. This step is directed at answering the RQ n.1, thus at providing a full scenario of high quality literature in this field and identifying the factors requiring further research. In particular, this systematic literature review (Cooper, 1989; Pettigrew and Roberts, 2006; Jesson, 2011) investigates the impact of different factors within HCOs on clinicians’ approach toward accounting instruments. The factors have been identified according to the common topics in literature and they refer to clinicians’ education, the patterns of collaboration between clinicians and controllers, and the characteristics of AISs. The paper highlights in particular the main findings in the field and sheds light on the relevant issues that will require further investigation.

The research considers articles published since 1980 in high-ranked peer review journals in the field of accounting, public sector management, and social sciences selected according to the rating provided by the Association of Business Schools Guideline 2015.

Based on the above literature search, 79 papers have been found. Each paper was synthetized and its main characteristics were identified.

The analysis of the results was first performed describing the characteristics of the articles, in terms of topics, trends of publication overs time, national and organizational contexts studied, and research methods. Then, the main findings have been presented based on the common topics emerging (Vaismoradi et al., 2013) and directions for future researches have been outlined.

3.2.2 Step 2: Case study

The second step of the research concerns the patterns of collaboration between clinicians and controllers in the implementation of AISs. It aims to investigate whether AISs design takes into account clinicians’ needs and answer to the RQ n. 2. Following the coercive control coming from regulations and its consequences on controllers’ identity in the organization, this step explores whether clinicians and controllers collaborate in the design of AISs. This aim relies on case study method.

This case study (Eisenhardt, 1989) has been developed in Italy, in a teaching hospital in Emilia Romagna.

Italy was considered the appropriate setting for conducting this empirical study because of the intense flow of managerial reforms that have pushed a change in the healthcare organizations and the coercive control on AISs design coming from regional and national government. In this sense, the strict national and regional laws about the information to be provided in AISs (Campanale et al., 2014; Macinati and Anessi-Pessina, 2014), contributes to question the model of accounting that the

21

Italian healthcare system has adopted since the beginning of the nineties. Moreover, the increasing national and regional control directed at benchmarking and comparability appears to reduce the capability of controllers to implement AISs for internal decision making (Järvinen, 2009; Fiondella et al., 2016).

In addition, the teaching hospital where this research has been performed is an autonomous, highly specialized and complex organization. The general director of the teaching hospital is appointed by the region, and the organization is funded based on DRGs: thus, the organization is accountable to the region, and a stricter link between the care activity performed and the revenues generated emerges.

Data was collected through interviews. Interviewees consist of 9 controllers and 11 clinicians responsible for health units, referring to different specialties. Controllers interviewed account for the total of information provided by the organization for both internal and accountability purposes; clinicians were selected according to their willingness to take part in the study.

Semi-structured interviews designed according to Alvesson and Willmott’s (2002) identity work framework were hold at interviewees’ workplace and focused on controllers’ perception of their role in the organization and the consequences on their capability to design AISs that fit clinicians’ needs. The overlapping between data analysis and data collection allowed adding themes emerging from the previous interviews to the interview protocol (Eisenhardt, 1989). Interviews were tape-recorded and fully transcribed, analysed assessing both within-groups and intra-groups commonalities and dissimilarities. Interviews were analysed based on Alvesson and Willmott’s (2002) identity work framework, to determine whether changes in controllers identity affect the design of AISs and, consequently, the capability of accounting instruments to fit clinician managers’ needs for decision making.

3.2.3 Step 3: Survey

The third step of the research concerns the capability of AISs to adapt clinicians’ information needs. The study considered both the HCOs structural configurations, in terms of centralization or decentralization of decisional processes related to the design of AISs (Malina and Selto, 2004; Abernethy and Bouwens, 2005; Chenhall, 2005), and clinicians medical education (Forbes et al., 2004; Jacobs, 2005; Torbica and Fattore, 2010). In this sense, this step is directed at answering RQs n. 3, 4, and 5. The aim of this step is to detect the extent to what clinicians perceive AISs adaptable to changes in care activity performed HCOs. Thus, the research aimed at understanding whether accounting instruments implemented in HCOs fit clinicians’ needs and whether structural configuration and medical specialization affect clinicians’ perception of AISs adaptability.

22

This step relies on a survey delivered to independent hospitals and Local Health Authorities (LHAs) hospitals in Italy. The survey has been delivered in six regions (Emilia-Romagna, Lombardy, Marche, Piedmont, Tuscany, and Veneto): all public independent and LHAs hospitals in these six Italian regions have been surveyed. The regions have been selected according to availability of data and the completeness of websites where email addresses of clinician managers were found.

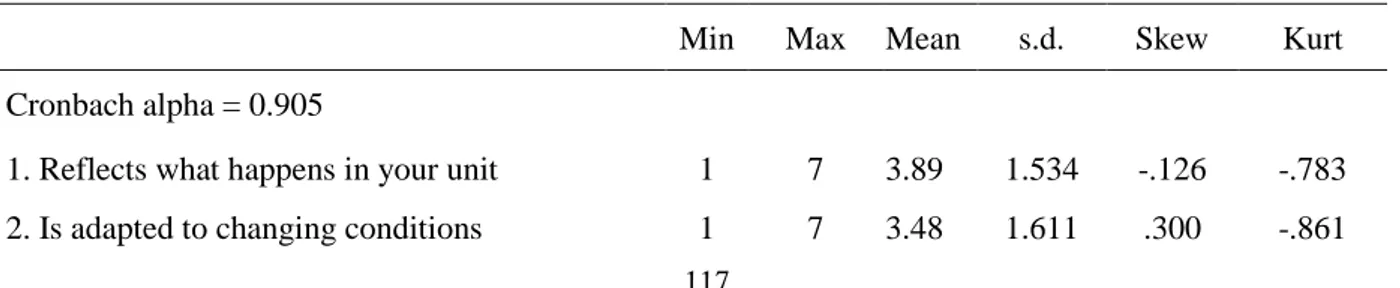

The questionnaire was designed based on the literature and on exploratory interviews hold in one of the independent hospitals object of study. The questionnaire included six items:

1. AIS reflects what happens in your unit;

2. AIS is adapted to changing conditions in the organization; 3. The adaptation to changes is timely;

4. AISs provide data related to cross-unit processes;

5. AISs provide information about new and innovative treatment; 6. AISs provide data about diagnostic and therapeutic pathways.

The latter three items (4, 5, and 6) of the questionnaire refer in particular to more patient-focused approaches. In this sense, simple inferential statistic conducted on data considered the whole group of 6 items first and then focused on the last 3 items, to assess whether differences in clinicians’ perceptions related to patient centric approaches could be detected.

The survey was based on a closed answers questionnaire managed through QUALTRICS software. The questionnaire was addressed to a population of 845 clinicians responsible for health units referring to six specialities: general surgery, gynaecology, internal medicine, geriatrics, and radiology. Focusing on the unit level is important, since clinicians are considered the primary users of resources; thus unit directors’ perception of cost accounting implications for decision making is to be considered relevant. 304 clinicians took part in the survey, leading to a response rate of around 36%. Questionnaires have been analysed and inferences assessed the impact of structural configuration and medical specialization on clinicians’ perception of AISs adaptability.

4. Findings

This dissertation aims to contribute to the literature concerning clinicians’ involvement in managerial activities in healthcare, and it provides an understanding of the factors that enhance clinicians’ resistance to AISs and suggestions about the implementation of AIS in HCOs. These regards, the research addresses accounting literature’s call for an investigation of the reasons hindering or exerting clinicians’ resistance to accounting in HCOs. In particular, the research focuses on the broad steam of literature in the field, and through a systematic literature review revises the literature published since the implementation of managerial reforms, it summarizes the

23

findings and identifies the mayor directions for future researches. According to these future research directions the remaining of this thesis has been developed. First, a case study analyses the patterns of collaboration between controllers and clinicians and highlights the attitudes of the two groups toward the cooperation in the implementation of AISs. Second, a survey directed to hospital clinicians provides a wider comprehension of the factors affecting clinicians’ perception of AISs adaptability to the care activity performed, and the role that medical education and structural configuration play in this sense.

4.1 Results from the literature review

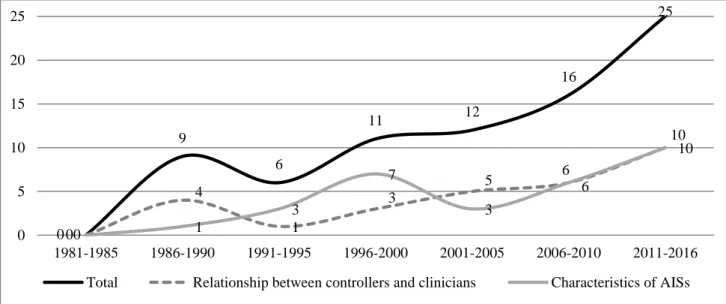

Considering the characteristics of the articles published in the field, literature addressed the topic mainly in accounting journals. Trends of publication show that literature paid growing attention to the topic over time, and that a great part of the researches (about one-third) has been published between 2011 and 2016. This suggests that, despite managerial reforms have been enacted in the early eighties, the theme is highly relevant to both academia and practitioners. Concerning the national setting, the European one is the mainly studied (73% of the researches), while above 80% of the studies deepened hospitals as organizational settings. Qualitative approaches are the more adopted (67%), followed by quantitative ones and few mix-methods studies. It emerges that literature investigated the theme over time mainly using qualitative researches in Europe and in hospitals. Therefore, need for future researches refers to the national and organizational settings that have been under-investigated and the use of quantitative methodologies, to ensure a broader approach and contribute to the development of accounting in the field.

Literature review underlines three main factors affecting clinicians’ resistance to AISs in HCOs: clinicians’ education and training, collaboration between controllers and clinicians, and the characteristics of the AISs implemented in HCOs.

With reference to the first factor, literature found that the medical education system, which traditionally not include managerial issues (Forbes et al., 2004; Jacobs, 2005; Torbica and Fattore, 2010), hinders clinicians’ comprehension of AISs potentialities for strategic purposes and decision making. This is because the medical education system enhances clinical autonomy (Forbes et al., 2004; Jacobs, 2005; Torbica and Fattore, 2010) and reduces clinicians’ willingness to be involved in management (Carlström, 2012; Elina et al., 2006). Furthermore, literature highlights managerial training can push a change in clinicians’ attitude: whether clinicians are trained to management, they increase their commitment to accounting and are more willing to be involved in management (Jacobs, 1995; Carlström, 2012; Macinati and Rizzo, 2014).

In this sense, literature emphasized the need to explore clinicians’ personal characteristics, such as gender, age, behaviours, and medical education, the impact of those characteristics on clinicians’

24

use of AISs, and the capability of managerial training to incentivise clinicians toward cost-containment strategies (Macinati and Rizzo, 2014).

The second factor identified refers to the patterns of collaboration between clinicians and controllers. In this sense, literature suggests that, being controllers the designer of AISs, they influence AISs according to their background and expertise (Naranjo-Gil et al., 2009, Macinati and Anessi-Pessina, 2014; Kantola, 2015). However, due to the differences between clinicians and controllers (Jones and Dewing, 1997; Forbes et al., 2004), the latter have frequently found difficulties in pushing a change in clinicians’ role, and in involving them in management (Kurunmaki, 1999).

Nevertheless, the integration of clinicians into formal structures of collaboration and the formal delegation of duties to them can helps in overcoming clinicians’ negative approach to AIS and push them toward a more proactive involvement in management (Abernethy and Vagnoni, 2004; Baker and Denis, 2011). When clinicians are successfully involved in managerial activities, and in particular in the design of AISs, they increase their willingness to assume managerial roles and to use AISs through a stronger commitment to organizational goals (Coombs, 1987; Pettersen, 1995; Jacobs, 2005; Scarparo, 2006; Lehtonen, 2007; Lachmann et al., 2013; Macinati and Rizzo, 2014). However, literature emphasizes the need to further explore whether the involvement of clinicians with controllers in the design of AISs is actually implemented in HCOs and which are its consequences on clinicians’ power and autonomy, as well as their capability to push a change in AISs (Østergren, 2009; Kraus et al., 2016).

Thus, the importance of involving clinicians in the design of AISs emerges, as clinicians’ perception of AISs scarce adaptability to their information needs is one of the main determinants of clinicians resistance (Forbes et al., 2004; Kippist and Fitzgerald, 2009; Pizzini, 2006). In fact, the inadequacy of AISs to fit clinicians’ information needs is an additional factor that exacerbates clinicians’ resistance to the use of AISs (Forbes et al., 2004; Kippist and Fitzgerald, 2009; Pizzini, 2006). Therefore, the third factor emerging from the review concerns the characteristics of AISs that are consistent with clinicians’ requests. In this sense, literature has advocated for the design of AISs that address clinicians’ needs to link costs with the care activity performed (Scarparo, 2006; Cherry et al., 2011; Szczesny and Ernst, 2016). However, literature reports only few attempts of AISs designed to meet clinicians’ request (Paulus et al., 2002; Vera and Kuntz, 2007; Demeere et al., 2009; Campanale et al., 2014; Hellman et al., 2015), while it emphasizes the advantages related to process-based AISs in supporting decision making and increasing clinicians’ commitment to accounting (Jacobs, 2005; Pizzini, 2006; Szczesny and Ernst, 2016). Future researches directions call for an investigation of both the characteristics of AISs that increase clinicians’ willingness to

25

accept their managerial roles and the capability of AISs to adapt to changes and contingency variables (Smith et al., 2005; Kippist and Fitzgerald, 2009; Börner and Verstegen, 2013; Pettersen, 2013).

4.2 Results from case study

The case study addressed the call for the investigation of the patterns of collaboration between clinicians and controllers in HCOs, on the light of the shift in power from clinicians to controllers observed by some authors following the coercive control coming from regulations (Jones, 2002; Järvinen, 2009; Fiondella et al., 2016).

Interviews conducted with both controllers and clinicians showed that the separation between the two groups that has been identified by accounting literature in the past (Mintzberg, 1983) is still far to be overcome. In fact, from the case study it emerged that the strict normative control on controllers’ activity resulted in multiple consequences. First, interviews with controllers revealed that the factors that guide the design of AISs are primarily related to the need to satisfy national and regional regulations directed at benchmarking among HCOs. Following the strict control on their activities coming from those regulations (Fiondella et al., 2016), controllers have changed their identity work and the perception of their role within the organization (Alvesson and Willmott, 2002; Järvinen, 2009). More in depth, normative requirements reduced controllers’ autonomy, strengthened their role as bean counters and the focus on the reporting activity (Friedman and Lyne, 1997; 2001). This bean counter attitude influenced controllers behaviours, and hindered their involvement in management (Vaivio and Kokko, 2006; Järvinen, 2009; Chiucchi et al., 2012) and their capability to perform a real managerial control in the organization (Pettersen, 1995; Granlund and Lukka, 1998; Kurunmaki, 1999; Järvenpää, 2007). Thus, controllers reported a commitment to the provision of accounting information that satisfy regulations, and a primary focus to address policy-makers requests.

Second, because of the change in controllers’ role, clinicians perceived AISs non-fitting their needs and reported that AISs are not clinical oriented and are designed only according to controllers’ purposes, thus accounting more for extra-organizational pressures than for internal purposes. Controllers interviewed recognized the need for a change in AISs directed toward the implementation of AISs that can support clinicians’ decision-making processes. Clinicians emphasized the importance of implementing AISs on a process-base, overcoming the existing vertical approach in accounting, claiming for a deeper involvement of clinician managers in the design of AISs. In this sense, controllers acknowledged the importance of satisfying internal information needs.

26

However, when asked about the actions to be performed to address clinicians’ requests, controllers reported a scarce capability to revise the design of the existing AISs. This is primarily due to the effects that regulations have on internal reporting, in terms of administrative burden and workload, which reduced the possibility to design additional AISs. Little space has remained in HCOs for an involvement of clinicians in accounting, being controllers mainly committed to the implementation of AISs that are based on normative requirements, and being subjugated to extra-organizational pressures for the provision of detailed accounting information consistent with national and regional requests. Therefore, the revision of controllers’ identity emerged in a scarce capability to involve clinicians in designing and implementing AISs that satisfy their information needs, as AISs are primary centred on supporting national requirements and benchmarking (Järvinen, 2009; Fiondella et al., 2016). The increased hierarchical top-down approach observed reduced the space for action at organizational level, and controllers’ capability to perform managerial control and to implement AISs that fit clinician managers’ needs (Jones, 2002; Guven Uslu and Conrad, 2011). Controllers are primarily focused on the provision of the data required by policy-makers, thus they fail to pursue a real managerial control, to help clinician managers in their decisional processes, and to reduce their resistance toward AISs.

The case study revealed that the characteristics of the existing AISs differ from the factors that would incentivise clinicians’ use of accounting information for decision making, as AISs are designed to satisfy different information needs. This enhances clinicians’ requests for a change in AISs toward the adaptation to the organizational changes and the care activity provided.

Although controllers recognized that AISs scarcely adapt to clinicians’ information needs, they showed a poor capability to design AISs that fit clinicians’ requests, and little collaboration between controllers and clinicians in the design of AISs emerges, because of controllers’ subjugation to normative requirements.

In this sense, findings suggested that the shift in power from clinicians to controllers in HCOs (Jones, 2002) has been overcome by an additional shift in power from controllers to policy-makers, which drove the implementation of AISs and the managerial control performed in the organization through regulations. Thus, an emptying of controllers’ activity occurred, following their loss of decisional power. Given the consequences of strict regulations on controllers identity (Järvinen, 2009), further research is required to investigate how HCOs can comply with regulations while also addressing clinician managers’ information needs.

4.3 Results from the survey

Designed on the bases of the literature and consistent with the results and the directions for future researches emerging both in terms of AISs design and clinicians’ education and training, the survey

27

conducted in the Italian setting allowed to deepen the knowledge about clinicians’ perception of AISs adaptability to the changes in HCOs.

More in depth, it explored the factors explaining clinicians’ perception of AISs adaptability in HCOs, with reference in particular to (i) the structural configuration of HCOs where clinicians operate, and (ii) clinicians’ medical specialization.

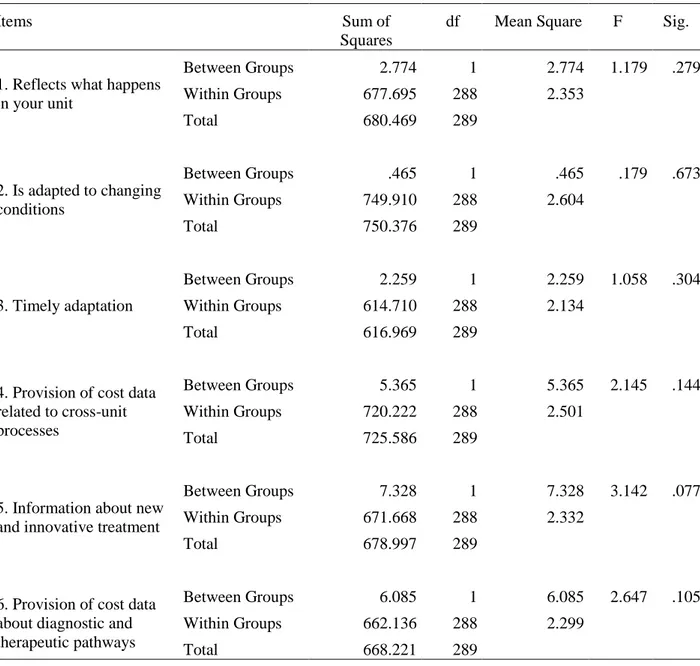

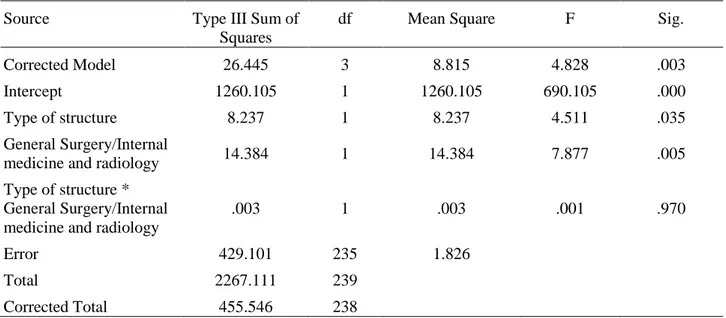

With reference to the first factor, the study aimed at understanding whether the structural configuration of HCOs (in terms of decentralization of decision making processes and information asymmetries) could impact on clinicians’ perception of AISs adaptability (Abernethy, Bouwens and van Lent, 2004; Abernethy and Bouwens, 2005; Pizzini, 2010). Expected results based on the literature were related to a perceived higher AISs adaptability in independent hospitals rather than in LHAs hospitals, because of the effect of the multiple services provided by LHAs, in terms of size of organization, increased information asymmetries and non-focus on the sole acute care (Uzzi, 1997; Abernethy and Mundy 2014).

Although these assumptions, results reported no significant difference between the two type of HCOs. This emerges probably because both independent hospitals and LHAs hospitals’ general directors are appointed by the region, are publicly financed and their AISs are defined at national level. This results in a common top-down approach in AISs design and in a commitment to meet more the needs of the regional government than clinicians’ ones.

However, the analysis conducted on the items 4, 5, 6 of the questionnaire (see Section 3), referring to more patient-focused approaches revealed that AISs in independent hospitals tend to adapt more to changes in care activity, suggesting that the structural configuration plays a role in this sense. This could be explained by the highly specialized activity provided in independent hospitals, where innovation is part of the organizational strategy. Further, the DRG-based funding mechanism in independent hospitals can result in a higher commitment to the provision of accounting data that are also process-based.

With reference to the second factor, the survey deepened the impact of medical specialization on clinicians’ perception of AISs adaptability.

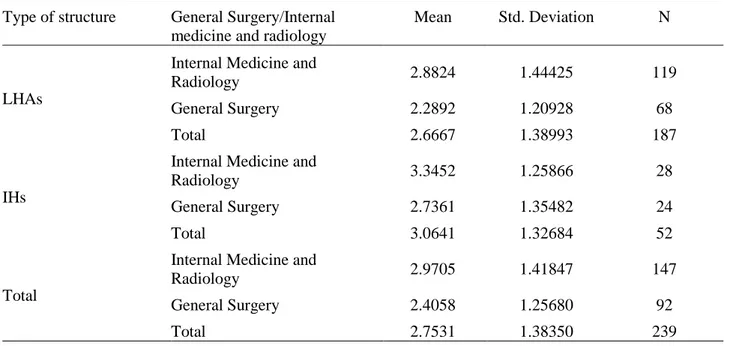

With reference to the second factor (clinicians medical specialization), literature argues that the type of specialization and personal characteristics affect the willingness of clinicians to be involved in managerial issues. In particular, this literature found that surgeons have a lower capability of to be involved in managerial issues and consequently a lower perception of AISs adaptability if compared to other clinicians (Gray et al., 1966; Schwartz et al. 1994).

Consistently with these expectations, the survey showed significant differences between surgeons and other clinicians’, both on the six items and on the three items scales, and surgeons’ constant