Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

D

IPARTIMENTO DII

NGEGNERIA DELL’E

NERGIA DEIS

ISTEMI,

DEL

T

ERRITORIO E DELLEC

OSTRUZIONIRELAZIONE PER IL CONSEGUIMENTO DELLA LAUREA MAGISTRALE IN INGEGNERIA GESTIONALE

Development of a Framework

to Estimate the Cost of Disposal

RELATORI IL CANDIDATO

Prof. Ing. Gino Dini Luca Cinti

Dipartimento di Ingegneria Civile e Industriale [email protected]

Ing. Nome Cognome Dipartimento di…

Ing. Nome Cognome Dipartimento di…

Sessione di Laurea del 4/12/2013 Anno Accademico 2012/2013

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

Luca Cinti

Sommario

Le aziende nell’Industria manifatturiera mirano, oggi, ad accrescere la loro conoscenza in materia di costi legati alla dismissione dei loro prodotti. I metodi di stima di tali costi sono, infatti, attualmente carenti ed inadeguati. Le incertezze e i rischi implicati nella dismissione vengono spesso trascurati, o per semplicità, si assume che quest’Incertezza possa variare la voce di costo di più o meno il suo 10%, seguendo una distribuzione triangolare. Il modello sviluppato fornisce il livello di informazione necessaria ad originare una più appropriata valutazione del costo di smaltimento per differenti industrie come: la Difesa, l’Aerospazio, la Marina, la Generazione Elettrica, il Petrol-Chimico e l’Automotive.

In questo progetto, l’analisi dell’incertezza e del rischio è stata incorporata nel modello in modo da catturare meglio le implicazioni del costo di dismissione, e allo stesso tempo consentire comparazioni tra scenari differenti. A ciò consegue un miglioramento del decision-making durante tutto il ciclo-vita del prodotto considerato. Questo lavoro di tesi è frutto dell’Individual project presso la Cranfield University compiutosi durante l’estate 2013.

Abstract

Manufacturing industries are very willing to grow their knowledge on the subject of Cost of Disposal. Indeed, they have a requirement to gain a greater understanding of the Cost of Disposal. Current cost estimation methods appear to miss out some of the uncertainties involved, or simply assumes a triangular distribution with a default setting of plus or minus 10%. The developed modello provides the necessary level of information to generate a more appropriate evaluation of the true Cost of Disposal for a range of industries, including Defence, Aerospace, Marine, Power Generation, Oil & Chemical and Automotive.

In this study, Uncertainty and Risk Analysis has been more fully embedded in the concept modello to better capture a greater number of Disposal Cost implications, whilst allowing comparison of differing cost scenarios. This will naturally improve the decision-making throughout the product Whole Life Cycle. The validation process provided the user company with a better understanding of the modello capabilities and, consequently, a greater confidence in Cost of Disposal predictions. The thesis represents the product of the Individual project at Cranfield University took place in the summer 2013.

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

ACKNOWLEDGEMENTS

First of all, I would like to thank Prof. Gino Dini, President and Professor of my Master’s in Manufacturing at the Universita’ degli Studi di Pisa. He is the one who offered me the chance to take part in the Double Degree Agreement between Cranfield and my Italian university, which provided me with a wide range of opportunities for the future.

I am also very grateful to my supervisor, Dr. Paul Baguley, for his guidance and his tenacious support. He helped me to do my very best and surpass the expectations set. I would also like to express my deep appreciation to the Industrial Contact, Cranfield University and the Academic Staff for being helpful and supportive throughout the entire year.

I am also indebted to Graham, above all a friend, colleague, and precious expert in Costs and Life. He, continuously, and generously shared with me with his knowledge, technical expertise, kindness and elegance, all of which makes him a true Gentleman.

Most importantly, I would like to thank my family, especially my mother, my father and my brother for their being support and the active role they have always played in my life. Particularly, I am grateful to my father, who has unceasingly contributed to my personal development with his insights, ideas, and teaching of ethics.

And last but not least, I would especially like to thank my grandmother, whose personality and enthusiasm forged my spirit, and who taught me to always turn my the eyes skyward.

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

TABLE OF CONTENTS

Sommario ... ii

Abstract ... ii

ACKNOWLEDGEMENTS ... iii

LIST OF FIGURES... vii

LIST OF TABLES ... ix

LIST OF EQUATIONS ... x

LIST OF ABBREVIATIONS ... 1

1 EXTENDED INTRODUCTION ... 2

1.1 Background ... 2

1.2 Context and Research Motivation ... 4

1.3 Aim and Objectives ... 5

1.4 Thesis Structure ... 6

2 LITERATURE REVIEW ... 9

2.1 Introduction ... 9

2.2 Disposal Process ... 9

2.3 The Role of Disassembly ... 12

2.4 Product LCC Analysis ... 15

2.5 Activity Based Costing ... 17

2.6 Uncertainty and Risk ... 18

2.7 Research Gap ... 20

2.8 Summary ... 20

3 MATERIALS AND METHODS... 22

3.1 Introduction ... 22

3.2 Stage 1: Understanding the context ... 22

3.3 Stage 2: Data collection and analysis ... 23

3.4 Stage 3: Framework development and validation ... 25

3.5 Summary ... 26

4 FRAMEWORK DEVELOPMENT ... 29

4.1 Introduction ... 29

4.2 The ROU Register ... 29

4.3 Distributions ... 32

4.4 The Scoring Mechanism ... 35

4.5 Monte Carlo Simulation ... 38

4.6 The Framework Logic ... 42

4.7 Summary ... 45

5 RESULTS ... 46

5.1 Introduction ... 46

5.2 Case Study ... 50

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

6 DISCUSSION ... 65

6.1 Introduction ... 65

6.2 Achievement of the Objectives... 65

6.3 Framework Modelling ... 65

6.4 Research Limitation ... 67

6.5 Summary ... 69

7 CONCLUSION AND RECOMMENDATIONS ... 71

7.1 Introduction ... 71 7.2 Conclusion ... 71 7.3 Contribution to knowledge ... 71 7.4 Future Work ... 72 7.5 Summary ... 72 REFERENCES ... 73 BIBLIOGRAPHY ... 75 APPENDICES ... 77 Appendix A - Questionnaire ... 77 Appendix B – Framework ... 81

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

LIST OF FIGURES

Figure 1 CADMID cycle ... 2

Figure 2 Product value gain [6] ... 3

Figure 3 Thesis Structure ... 7

Figure 4 The disposal and disassembly process ... 10

Figure 5 Disassembly families ... 12

Figure 6 Determination of optimal Disassembly strategy ... 13

Figure 7 Iceberg metaphor ... 16

Figure 8 Research Methodology ... 27

Figure 9 ROU Register ... 30

Figure 10 Example of Uncertainty item... 32

Figure 11 Distributions ... 34

Figure 12 Scoring Card ... 36

Figure 13 Uncertainty Impact ... 38

Figure 14 Three distributions (Triangular in green, Uniform in blue, Gaussian in red) ... 39

Figure 15 Distributions Input ... 40

Figure 16 Monte Carlo Simulation ... 41

Figure 17 Cost Distribution ... 42

Figure 18 Framework Logic Flowchart ... 43

Figure 19 Survey's Results ... 46

Figure 20 IDEF of General Disposal process ... 48

Figure 21 Life Cycle Cost Analysis of an aircraft F-35 ... 49

Figure 22 Example of scoring mechanism compiled ... 52

Figure 23 Figure 13 The Uncertainty Impact card and the new scale (for Total Score>50%) ... 57

Figure 24 The Uncertainty Impact card and the new scale (for Total Score<50%) ... 57

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

Figure 26 Monte Carlo Simulation: three different samples of distributions (above) and the total Disposal Cost PDF output (bottom) ... 61 Figure 27 Monte Carlo Simulation Results ... 62

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

LIST OF TABLES

Table 1 Factors affecting the product disassembly [3] ... 14

Table 2 Product recovery options after disassembly [10] ... 15

Table 3.1 Interviewee profiles ... 25

Development of a Framework to Estimate the Cost of Disposal – Luca Cinti

LIST OF EQUATIONS

Equation 4.1 σreadjust (for Total Score>50%) ... 56 Equation 4.2 σreadjust (for Total Score<50%) ... 57 Equation 4.3 function of cost ... 60

LIST OF ABBREVIATIONS

BoM Bill of Materials

CADMID Concept, Assessment, Demonstration, Manufacture, In service, Disposal

CDF Cumulative Distribution Function

CLT Central Limit Theorem

DFD Design for Disassembly

DoD Department of Defence

EOL End-of-Life

EPSRC Engineering & Physical Sciences Research Council

FP7 7 th Framework Programme for Research and Technological

Development

HSE Health and Safety Executive

GAO USA Government Accountability Office

IDEF Integrated Computer-Aided Manufacturing DEFinition

LCC Life Cycle Cost

LRU Line Replaceable Unit

LT Long Term

MOD Ministry of Defence (UK)

NASA National Aeronautics and Space Administration NATO North Atlantic Treaty Organisation

NAVSEA Naval Sea Systems Command

PDF Probability Distribution Function

ROU Risk Opportunities and Uncertainties

SCAF Society of Costs Analyses and Forecasting

SCEA Society of Cost Estimating and Analysis

1 EXTENDED INTRODUCTION

1.1 Background

Disposal has not historically been an issue for legacy Defence products and projects.

The Disposal process, which may also be referred to as Disassembly, Decommissioning, or Deactivating represents all those activities required to retire a particular product line [1].

The focus of this project is the last step of the CADMID (Concept, Assessment, Demonstration, Manufacture, In service, Disposal) life cycle, as shown in Figure 1:

Figure 1 CADMID cycle

The main areas of interest in this work have been on the topics of: Disposal Process, Uncertainties and Risks Analysis and Disposal Cost Estimation.

The Disposal stage is usually quite a different process compared to the preceding stages of the CADMID. This is a consequence of the often unique and sometimes exceptional conditions of the product at the end-of-life stage (i.e. damaged parts, joint deterioration or oxidation) [2].

Due to the poor and narrow margins obtained from the considered process, it does not justify an accurate estimation of the costs. As a result, the disassembly plans seems to be undervalued and more inaccurate compared to the manufacturing ones. Moreover, the time existing at the end of the product life cycle tends to produce imprecise decision-making, which does not allow for a proper cost-benefit analysis of the disposal process [4].

These days, manufacturing companies are more concerned with the topic of disposal than in previous years. This is due to the current pressure from

or recycling of the product materials), to meet new environmental standards and so to minimize the impact of the disposal outputs (i.e. scrap, waste materials and energy use) [5]. Moreover, in the past equipment was bought, nowadays it is leased, hence the suppliers have to dispose of the asset they manufactured.

On the other hand, there is a new awareness to the opportunity of gaining value from the product scrap.

Joshi et al (2006) theorize that changing the company from 3R approach (reduce, reuse, recycle) to a 6R approach (reduce, remanufacture, reuse, recover, recycle, redesign) it will allow direct and tangible benefits to the business, as shown in Figure 2 [6]:

Figure 2 Product value gain [6]

The Defence industry is currently dealing with the disposal of their products in a different and specific manner from other industries such as Automotive, Marine, Nuclear and Oil & Chemical. In fact, Defence companies now commonly deal with long-life complex equipment, which needs to be disposed of 30 or 40 years after the Design and Development phase.

For instance, the Cost of Disposal impacting on the life cost of a F-35 military aircraft is estimated at around 43,000,000 of Canadian Dollars, compared to the

This range of outcomes, even though they represent a low percentage of the entire expense, can easily be greatly under or over estimated at the early stages of the CADMID whole life cost evaluation. Unfortunately, most legacy projects do not have any existing estimates for comparison.

Significant under or over estimation is a real risk when the cost of Uncertainties and Risks are neglected during the cost evaluation stage.

Uncertainties and Risks can substantially affect the Whole Life Cost estimates, meaning actual costs significantly differ from those expected (General Accounting Office, USA, 1997). For that reason, risk management cannot be ignored at the early stage of the CADMID Whole Life Cost estimation, in fact, estimates are insufficient as a basis for sound decisions when considered alone, especially for multi-year product life-cycles such as those for military aircraft or a naval vessels.

Donald Rumsfeld, while serving as United States Secretary of Defence in February 2002, states in reference to definition of types of risk [7]:

“There are known knowns; there are things we know that we know.

There are known unknowns; that is to say, there are things that we now know we don't know.

But there are also unknown unknowns – there are things we do not know we don't know.”

This framework attempts to assist the Disposal Cost Estimator with the inclusion of information that is known, but also, and especially, greater awareness of the last categories, namely: the known unknowns and unknown unknowns. This will provide the business with a more truthful and realistic cost evaluation.

1.2 Context and Research Motivation

What are the commonalities between the different disposal processes in different industries?

What is the total cost associated with the product End-of-Life cycle? and how is this currently evaluated?

Do standards for cost estimation of Disposal Costs exists?

Are the Disposal Cost Uncertainties, Risks and Opportunities related?

How can the concept of Risk, Uncertainty and Opportunity be embedded in the Disposal Cost evaluation?

The current estimation process for the Cost of Disposal within the Defence industry tend to use specific estimates based on information known:

o the Line-Replaceable-Units (in the Defence terminology, LRUs represents the analogue of the product Bill of Materials);

o the set of contract requirements for the product disposal;

o the identification (and quantification where appropriate) of what is not yet covered in the estimates (DAREO: Dependencies, Assumptions, Risks, Exclusions, Opportunities).

To reduce consequential under / over estimation of Risks, Uncertainties and Opportunities, Cost Engineers in the Defence industry (example considered in the thesis), assume a triangular distribution of the costs with a default setting of plus or minus 10%.

The Generic Framework aims to address the concerns identified and to resolve the current short-comings in the process of evaluation of Cost of Disposal for the Defence industry.

1.3 Aim and Objectives

The aim of this project has been to develop a Generic Framework for estimation of Cost of Disposal with Uncertainty and Risk, identifying requirements and best practices.

To identify and compare the existing disposal procedures of complex products through the analysis of the literature, supported by interviews with expert in the field

To develop a framework that provides the necessary level of information to generate a more truthful evaluation of the costs involved in the disposal processes

To validate the developed framework by means expert review

1.4 Thesis Structure

This thesis comprises seven sections, and its structure is represented in Figure 3. A beginning chapter (1) called Extended Introduction is carried out to explain the context and the Research Motivation.

Section (2) states the review of the literature related to the project. It includes several topics, which directly influenced the project, such as the Disposal Process, The Role of Disassembly, Product LCC Analysis, Activity Based Costing, Uncertainty and Risk and the review of previous work and the investigation of potential gap in the literature.

Section (3) explains the materials and the methods applied on the project and the actions undertaken.

Section (4) is detailing the development of the project and of the Framework, from data collection to the model, including the Logic and how each component of the tool was developed

Section (5) disserts about the results of the project, highlighting a Case Study and the Validation trough experts’ judgment. In Section (6) Results are discussed and Research Limitations stated.

2 LITERATURE REVIEW

2.1 Introduction

In the following chapter is described what the results of the literature review are. The disposal process in macro perspective is discussed (3.2) and how, nowadays, the role of disassembly is becoming a relevant support to the decision making (3.3).

Finally, the cost of disposal estimation represents a part of the product Life Cycle Cost analysis 3.4 and jointly with Uncertainty and Risk is treated in this project 3.5.

2.2 Disposal Process

As earlier mentioned the Disposal process represents all those activities required to retire a particular product line [1].

With the term Disassembly, which represents a part of the whole Disposal process, is intended the process of physically separating a product into its parts or subassembly pieces. [4]

Numbers of different studies about the topic, nowadays, aims to resolve and facilitate the Disposal effort, such as the Design for X (DFX).

This is a collection of methodologies, which allow the correct evaluation of several product characteristics and requirements at the earliest stage of the product development phase by enclosing several design aspects (i.e. assembly, disassembly, manufacturability, etc.) [17].

A research on define a common disposal process which is able to generalise the process for every industry have been undertake. In Figure 4 it is simplified and represented.

It is a clear understanding that after a first products collection process the product has to be sorted into disassembly families thanks to the sortation facility. Then the disassembly employers following a documented disassembly

procedure will return the product disassemble in the different way available (recyclable material, reclaimed parts or landfill) [4].

Figure 4 The disposal and disassembly process

The investigation also shows that two different kinds of disassembly facilities exists [4]:

1. All those facilities that work directly or indirectly with OEM (original equipment manufacturer)

Moreover, it is interesting to underline that the disassembly process can be categorized into two different methods of disassembly [10]:

1. Destructive, when an irreversible disassembly operation destroy the product or the component

2. Non-destructive, when there is no irreversible transformation

The second family can be also classified in:

1. Total disassembly, when the full product is disassembled into small components

2. Selective disassembly, where a complex product is reversible disassemble into less complex parts

Generally, the disassembly process includes different options for different scenarios. In the Figure 5 are represented all the possible options classified, firstly, by the dismounting process and, secondly, by the process output. It is important to distinguish the meaning of each of them:

• Reuse: usage of the EOL components for the same purpose of their original conception;

• Recycling: reprocessing disposal scraps for the original purpose or for other purposes, but excluding energy recovery;

• Remanufacturing: reprocessing of the EOL product at the module level. The process aims to recovery the product just replacing certain obsolete module.

Regarding the disposal process there is also the possibility to landfill the wasted parts:

• Energy recovery: incineration of combustible wastes, as such or mixed with other waste, with heat recovery.

Figure 5 Disassembly families

2.3 The Role of Disassembly

As mentioned earlier, it is important to make choices that help the disassembly of the system (Design for Disassembly) at the early stage of the product design. As a consequence, It is also relevant to pursue the best disassembly sequence (Disassembly Sequence Planning).

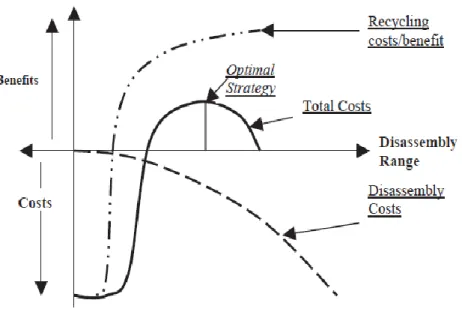

As we can see in the Figure 6, the optimal strategy is obtained as a trade-off between the minimization of the disassembly costs function and the

Figure 6 Determination of optimal Disassembly strategy

In literature, Disassemblability has been defined as the degree of easy disassembly [10]. Disassemblability is drive by factors such as [4]:

Disassembly time, represents the total time spent since the disassembly process start until the operation is completed

Use of tools, whether is required a special or OEM’s tool or an air gun it is enough

Fixture required, sometimes the disassembly can be accomplished with the only use of two hands or in other occasion that is required an

automatic fixture

Access, it is different a disassembly along the Z-axis direction then one operation that is not even visible

Instruction, proportional to the training and the expertise needed for the operations

Hazard, as the treatment of toxic materials

Force, as minimum is the force required easier will be the disassembly process.

Moreover Justel Lozano and Daniel (2009) [3] collected other factors that affect the product Disassemblability and the related DFD strategies.

Table 1 Factors affecting the product disassembly [3]

Important to underline, that the disassembly process cannot be just considered the reverse process of the assembly operations [2].

The reasons are that the product at the end of the life cycle can be different from the original one. Also, non-reversible joint (gluing for example) permanently modify the product. Sometimes the disassembler could considered more profitable the destructive operation (landfill/incinerate). As a consequence, the reversing the assembly sequence (the Bill of Materials for example) is not always economically convenient.

Table 2 Product recovery options after disassembly [10]

2.4 Product LCC Analysis

The CADMID cycle, as described earlier, drives the Product Life Cycle Cost analysis (LCC).

LCC, in fact, should ensure that all the costs have been properly taken into account and these should be the minimum in order to match the customer satisfaction. As Massimo Pica suggested [1], the costs come from the translation of the technical requirements and project parameters considered.

Agreeing to the ISO (2006) the Life Cycle Assessment is a procedure to evaluate the potential economic and environmental impact throughout the whole product life. Moreover, it aims to understand and evaluate the magnitude of the potential system capability.

According to the iceberg metaphor (B.S. Blanchard, Figure 7), it is explained the different visibility of the LCC factors. As we can see in Figure 7, a poor management will not be able to appreciate the sunk costs in the bottom of the iceberg. That should make you think over, that the assessment of cost of disposal is not particularly simple and even evident.

Moreover, it is important to underline that the major costs compare with the total cost are the one that come from decision made at the early stage of the CADMID.

Figure 7 Iceberg metaphor

From a macro point of view, the LCC could be the result of the sum [1]: 𝐿𝐶𝐶 = 𝐿𝐶𝐶𝐴 + 𝐿𝐶𝐶𝑂 + 𝐿𝐶𝐶𝑅

Where LCCA represents the Life Cycle Cost of Acquisition, LCCO is the Life Cycle Cost of Ownership and LCCR is the Retirement (Disposal) Life Cycle Cost.

In depth, LCCR is driven by:

Where CRS is the Cost of the system Shutdown, CRD is the Cost of the Disassembly process and CRR is the Cost of the Recycling process.

The top-down logic can be follow until we rich more details in the cost structure. The idea, in fact, is to breakdown the LCC into smaller cost component until we reach the detailed level desired.

In the case of disposal process could be interesting to switch the point of view from the minimization of the cost to the maximization of the profit. Hence, we could consider the corresponding revenues of each disassembly action. For example a destructive action will negative affect the function where instead the value of a recyclable material will positive influence the function [2]

2.5 Activity Based Costing

According to LCCA different product cost estimation techniques have been developed so far.

They can be classified in qualitative and quantitative and they can be differently used depending on the purpose [18]. The qualitative techniques are strictly related with the past experience which the company gained with previous similar project. They are based on intuitive assessment such as the judgement of an expert, or they can be based on the regression analysis of past data. On the other hand the quantitative techniques are referred to evaluation of the product features and the production behaviours (parametric) or the identification of analytical function drive by certain variable.

Activity-Based Costing (ABC) has received more attention during the past years. This is because of its capability to trace the costs, to separate the indirect from the direct costs and for the its high accuracy [19].

The ABC’s technique is a conventional cost system based on the idea that production processes consume activities and not resources (labour, energy and materials). Moreover, differently from others techniques, ABC allows the cost

estimation on the unit-level cost driver (i.e. machining time, direct labour in hours).

Figure 2.8 Product Cost Estimation Techniques

2.6 Uncertainty and Risk

Nowadays, one out of four project succeed, a third usually will stop before the completion and almost 50% shows different problems along the life because of unexpected risks.

Commonly, we use to define the risk as the negative effect that could affect an uncertain situation.

Whereas uncertainty is a stochastic situation that cause indefiniteness and lack of certainty of outcomes.

probability while uncertainty causes randomness with unknown probabilities (Hillson D, 2009).

The variation can become a risk when is negative affecting the project, or an opportunity whether is positively influencing the project.

Risk in a project could be identified with well-known techniques such as:

Delphi

Brainstorming

SWOT analysis

Checklist

Cause-effect diagram

These methods need to feed by certain input information as:

Problem description Context description Project Objectives Project requirements Constraints Parties involved Solution Resources committed Project plan Historic information

Every risk is described by a likelihood value that shows the probability of occurrence and the impact value, which will, represents the potential damage of the risk.

𝜌 = 𝑝 × 𝑑

Where 𝜌 is called the risk exposure, 𝑝 is the probability of occurrence and d is the potential damage.

2.7 Research Gap

A lack of information and practices on the field drives this project to promote a research on the Risk and Uncertainties related to the estimation of the cost of Disposal.

it is noteworthy to mention that the literature review underlined that the Disposal Process represents, nowadays, a relevant topic for companies in different industries. This is due to the new government legislations and because of the cost saving policies.

It is, in fact, important to consider the topic of Disposal since the beginning of the product LCC Analysis, as this will influence the total cost of the project at the end. On the other hand there are no standards which can drives the companies and a lack of common practice can be applied in different industries.

This is because companies neglected or ignored that the Disposal effort is are costs which need to be accurately assess.

The accuracy of these costs struggled to be properly considered, as we can imagine the cost of Disposal of an aircraft which will be dismantled 40 years after its Manufacturing. The long run horizon occurring between the Manufacturing and the Disposal drives the uncertainty in the cost.

Consequently, the research focused on reviewing the practice of cost estimation which embeds a Risk and Uncertainty evaluation.

No standard or relevant cases have been found. Moreover the actual process to consider the variance in cost seems to be poor and imprecise.

2.8 Summary

The disposal process is nowadays a topic of concerning for diverse reasons.

Companies are now focus on the role plays by the disassemblability and the capacity to influence this effort from the beginning of the product Life Cycle.

As the research gap evidence, a lack of knowledge on how to embed the uncertainty and risk in the cost assessment have been identified.

3 MATERIALS AND METHODS

3.1 Introduction

This section provides an overview of the materials (sources of information) and methodological approach taken to develop a flexible Framework which is able to support a more comprehensive estimation of Disposal Costs.

As shown in the Figure 8 (at the end of the chapter), the project was progressed in three stages:

1. Understanding the context

2. Data collection and analysis

3. Framework development and validation

It is worthwhile mentioning, that because of obvious constraints of the Masters project timeframe, an Agile Development of the project has been adopted. The principal being, that development of the Framework can be carried out iteratively and incrementally, thereby solving problems and developing ideas that are highlighted through review and use by third parties (including Industry Experts and Academia) [15].

3.2 Stage 1: Understanding the context

A review of more than 60 papers, concerning Disposal Context, was carried out. The literature was accessed with support of academic databases such as Scopus, Google Scholar, Science Direct, Elsevier Science Journals and Emerald Journals, in addition to sources which belong to FP7, EPSRC, DoD and NAVSEA.

The research aimed to investigate the current understanding and practice of the following subjects:

the Uncertainties and Risks management in a project

Following the information review, a literature report has been compiled to highlight the As-Is situation and to outline the literature gaps.

3.3 Stage 2: Data collection and analysis

This stage aimed to gather the information needed to conceptualise the Framework.

As a consequence, techniques and methodologies to assess the Cost of Disposal and to embed the uncertainty element have been analysed.

A semi-structured questionnaire was created to be used with Academia and Industry experts in order to explore the companies’ requirements and to better understand the issues surrounding their Disposal of complex products. In particular, one the major defence contractor has been the main stakeholder of the research.

The questionnaire born with the aims to gather the different expertise of major experts in the Manufacturing industries.

Consequently, the questionnaire was structured with several open questions in order to give the interviewee with the chance to freely answer the question and listen at their point of view.

The questions elaborated were drives by the curiosity to know more in detail about the Disposal topic and to gain an overall understanding of what are the research gap and industry concerning. They were suggested by the concerning found in the Literature review and from the support of academia experts.

The use of pilot questions such as:

o Are there any standards to estimate disposal costs?

o Do you have specific cost models to estimate disposal cost? and are

they Excel based or Proprietary Cost Models?

o Are the cost models detailed, analogous or parametric?

o Will a generic cost model for disposal cost estimating help your

business?

o What are the current requirements to estimate disposal costs? o What are the actual / common disposal process?

o Which are the key factors of the process? o Which areas are lacking key data?

o How accurate are current disposal cost estimates?

As a consequence, several face-to-face interactions with experts in Sustainability, Electrical Utility Industry, Re-manufacturing, Automotive and Defence were undertaken.

The summary of the interview results is summarised in the Section 5.1 of the thesis.

Table 3.1 Interviewee profiles

During this stage, there was the opportunity to participate in the workshop: “Quantitative Cost and Risk Analysis” organized by the Society for Cost Analysis and Forecasting (SCAF), an association of industry experts in cost analysis that aims to share knowledge and thoughts concerning Cost and Forecasting methods.

3.4 Stage 3: Framework development and validation

Stage The third stage aimed to develop an innovative Framework, using the Microsoft Excel spread-sheet format, populated with the data previously collected.

Finally, the Framework tool was critically validated and improved upon, thanks to the judgment of two major experts in this field, these being; a Head of Risk & Opportunity Management and a Head of Estimating. In particular the use of the tool was demonstrated using a hypothetical case study.

3.5 Summary

This chapter aims to give a top level definition of the project. For this purpose, it has been defined what were the stages followed during the whole project. As earlier mentioned, the Figure 8 graphically summarised the process followed step by step.

4 FRAMEWORK DEVELOPMENT

4.1 Introduction

The Framework was designed in a Microsoft Excel spread-sheet format, and comprises the following areas (as ordered in the spread-sheet):

The Framework Logic

ROU Register

Distributions

Scoring Mechanism

Monte Carlo Simulation

This section details how the elements above were developed. It is worthwhile mentioning that in order to simplify the explanation, the sections below followed a different order compare to the order followed by the Framework spread-sheet.

4.2 The ROU Register

During the initial period of the Framework development, familiarisation of the Uncertainties involved in the disposal process was necessary. This process required collection and analysis of diverse types and categories of Uncertainties from more than 100 published documents within the scientific domain.

More attention was dedicated to those papers from the Defence sector, such as publications from the MoD, NATO, SCEA, SCAF, GAO, DoD, and NASA [13]. A “Risks, Opportunities and Uncertainties Register” was then populated with around 100 different uncertainty items related to the disposal needs of Defence projects. The register was then categorised as shown in Figure 9:

Figure 9 ROU Register

The range of Uncertainties was derived from the review of literature, with each document being read and analysed to identify the data sought. The main focus was to clearly describe the definitions of Risk and Uncertainty

According to the BAE Systems Integrated System Technologies definitions [11]: o “Risk - An event or a series of events which, on occurring, would damage a

project objective in terms of performance, functionality, time of delivery, acceptance, or cost.

o Uncertainty - The range of outcomes associated with estimating work; an attribute describing the possible spread of cost or duration, due to the availability of information on the task itself or the estimating method used.”

Throughout the whole Framework development process, ‘Risk’ has been considered a discrete event that might or might not happen and, should it happen, could affect the cost in differing ways in terms of impact and / or frequency. In addition, ‘Uncertainty’ has been considered a likely source of real

variation that will affect the cost estimate, especially its variance from the perceived likely value.

As previously stated, the ROU Register was simply constructed in a Microsoft Excel spread-sheet format, where the main column identifies the “Type of

Uncertainty”, in light-grey colour. The ‘green’ columns (in the figure just two of

them, from the left to the right, are highlighted) provide:

- Description/Info - this column provides a simple definition of what is meant on the related ‘Type of Uncertainty’ cell

- Examples - examples of different Uncertainties are described here

- Examples of Risk - examples of risks, relevant to the Uncertainty considered, are described here

- Opportunities – this column identifies the Cost Opportunities relevant to the risk considered. Each opportunity details realistic occasions possible for each specific situation of risk

- References – for each type of Uncertainty, information sources have been provided.

The categorization, represented by the left grey columns (in Figure 6), were actually proposed by industry experts (detailed in Chapter 2) as the most efficient way for the Framework user to sort information required during the assessment process. From the right to the left:

- Sub-category – this categorisation clusters the Uncertainties depending on where / which business area will be affect by the Uncertainty considered? - Category – provides a secondary ‘macro’ search category

Thanks to the approached Agile Development (as described in Chapter 2), the Framework concept has evolved from a mere Uncertainties Register into a scoring Framework able to support the Cost Engineer during the assessment of the Cost of Disposal.

4.3 Distributions

As the aim of the project was to deliver a Framework able to support the cost Engineer at the earlier stage of the LCC, it has been considered that costs can undertake different behaviours. In fact, because their nature of variance, costs need to be assume under certain probability distribution.

A probability distribution function (PDF) is a continuous function which represents the probability (or the likelihood) of a certain variable to happen on a choose event.

As mentioned, the PDF helps the assessor to provide more reality and precision to the cost evaluation. This is because, different PDF with different continuous function can better fit the nature of this cost elements.

An investigation on the possible different existing PDF drives a collection of each of them in the spread-sheet called “Distributions” embedded in the final Framework.

Thanks to the work of Chris Rodger and Jason Petch [14], each type of PDF is detailed with:

Example of distributions, it graphically represents the shape of the

ID Category Sub-category Type of Uncertainty Description / Info

3 Legislation Current Government restrictions, Regulation

electronic scrap as well as handling of hazardous materials and disposed waste have to be carried out according to the existing laws.

Use, it explained the behaviour and the constraints of the PDF;

Situation where suitable, it represents a suggestion to the user for the condition usage;

Examples, this section aims to provide the user with example when a certain PDF is fitting the most.

All the information above are finally collected in the PDF database as shown in the Figure 11:

Developed by: Luca Cinti, 2013

Type Example distributions Use Situations where suitable Examples

Triangular

This is the most commonly used distribution. It has no theoretical justification; however, it is a very simple and clear distribution to use. Note that it overestimates the

size of the tails at the expense of values close to

the mean.

Where the distribution is not known, and it is thought not suitable for a normal distribution, either because it

is boundedor because it is

not symmetrical. Situations where a simple intuitive understanding is paramount and flexibility is a

great advantage.

The operational maintenance costs of a project have been estimated as being a minimum of £40k, with the most probable £60k and a maximum of £100k. The

actual cost could be modelled as a triangular distribution.

Note that the mean, or expected value, of a triangular distribution is not the most probable value, but is in

fact given by:

mean = (minimum + most probable + maximum)/3

Normal/Gaussian

Another frequently used

distribution. This is in part

due to the result of the central limit theorem which states that the mean of a set

of values drawn independently from the same

distribution will be normally described. Many distributions tend towards normal at their limits (e.g. Poisson and binomial).

Many natural variables fall into a normal distribution, such as human heights (male

or female), elephant weight etc.

Distribution of errors

A situation where the

distribution is not known, but it is known to be symmetrical around a mean value, and more likely to be near the centre than the

extremes.

The retail price inflation has been assumed to be 3% per annum. However there is a chance that it could be above or below this rate. The mean here is 3%, and the standard deviation (s) should be estimated bearing in mind that the probability that a value falls within:

+/- 1σ of the mean = 68% probable +/ 2σ of the mean = 95% probable +/- 3σ of the mean = 99.7% probable

Uniform distribution

Used if the variable is

bounded by a known maximum and minimum, and

all values in between occur with equal likelihood.

Like the other nonparametric distributions, this has the advantage of being

intuitively obvious, and highlights the risk as one where there is very little information about its

distribution.

The position of a leak along a pipeline, or the price at any given point in time of a highly market sensitive

commodity such as petrol.

Binomial

For each trial there are only two outcomes (i.e. pass/fail,

heads/tails) The trials are independent:

what happens in one trial does not affect the

subsequent trials The probability remains the

same from trial to trial

This should be used if you

require the number of events that will occur given a certain number of trials and a

known probability of occurrence.

You want to describe the total number of defective items in a sample of 100 manufactured items, given that the probability of any one item being defective is 7%. The number of defective items will be given by a

binomial distribution with n=100, p=0.07.

Poisson distribution

The rate of occurrences remains constant

The number of occurrences is not limited

The occurrences are independent

This discrete distribution describes the number of events that will occur in a given unit of time, given that

the rate is known.

If there is a performance measurement system that deducts payment every time a failure occurs, and it is assumed that the rate of occurrence will be 20 times a

year: the number of such events that occur in a given quarter will be described by a Poisson distribution with

a rate of 20/4 = 5/quarter.

Exponential

Describes the amount of time between occurrences

The rate of occurrence is independent of previous

occurrences

Only used for describing the time between (or until)

occurrences.

If destructive tests show that a light bulb lasts on average 5200 hours, how long a given light bulb will last will be described by an exponential distribution if we further assume that the rate of failure is constant (i.e. the chances of it failing are the same throughout

its life).

Log normal

This distribution is also used reasonably frequently. The central limit theorem states that if a quantity is the product of two or more independently chosen variables, the distribution

will tend to log normal.

Naturally occurring variables that are themselves the product of a number of naturally occurring variables.

Any variable that extends from zero to +infinity and is positively skewed. Useful for

representing quantities that vary over several orders of

magnitude.

The volume of gas in a naturally occurring gas reservoir is often log normally distributed, being a product of its volume, pressure, gas/liquid ratio etc.

Beta distribution

Used to determine the probability of an event given

a number of trials n have been made with a number of

recorded successes r. This distribution is primarily used to extrapolate the data taken from a sample to the whole

population.

If you only have a limited set of data and have to generate a probability distribution from them. Note that this gives a distribution of the probability of an event or series of events, rather than how many events will occur.

If in 100 (n) firings of a gun, it mis-fired 16 (r) times, what is the probability that it will misfire? Use Beta(17, 85). This also works for estimating cases where there have been no misfires (i.e. r = 0) provided

there is some chance of failure.

σ1 = r + 1; σ2 = n - r + 1

Reference: Uncertainty & Risk Analysis

by Chris Rodger and Jason Petch

BUSINESS DYNAMICS April 1999

http://clem.mscd.edu/~mayest/Excel/Files/Uncertainty%20and%20Risk%20Analysis.pdf

It is important to select the suitable probability distribution to represent the aggregated cost drivers:

4.4 The Scoring Mechanism

Concurrent with the population of the ROU Register, a Scoring Card was conceived. This, in fact, aims to embed the Uncertainties of each Cost Estimate using a simple and flexible mechanism, which allows the user to obtain a more accurate evaluation of the cost. In particular a method was developed to modify the uncertainty from a plus or minus 10% variation in a symmetric triangular distribution.

It provides a simple, intuitive and flexible tool that can easily be adapted for an estimation of another stage of the product Life Cycle. It can even be adapted for the same disposal process, but for a different industry such as the decommissioning of a nuclear power plant or the disposal of hazardous materials.

The output of the Scoring Mechanism delivers a reshaped cost distribution. In other words, the statistical distribution of the cost will be more widely readjusted, should the Uncertainty suggests a larger impact than simple adjustment │±10%│, or more narrowly readjusted were the outcome suggests a lower range than a simple│±10%│adjustment of the total cost element.

Here, again, the analysis of the requirements through interactions (i.e. teleconferences, e-mails) with the user company were noteworthy to comprehend how to structure and logic the scoring card.

The main requirements identified with the partner’s participation were: To add value to the company

To innovate the defence business and the current literature about disposal

To provide a Disposal Cost Estimating Tool that simple in terms of effort and process time

Figure 12 Scoring Card

As can be seen, within the Scoring Card illustrated above, this is divided into different colour areas.

The first three blue columns on the left require user input:

- Cost Element – this is the name of the cost element (from the Line-Replaceable Units, Air Platform) considered

- Uncertainties Involved (ID) – each one of the Uncertainties considered to have high impact on the cost, should be listed here

- Evaluation approach – the user is asked to input information about the source and how the evaluation will be carried out. Different approaches have been identified in the literature, one of two approaches may be selected in the card [8]:

o The Deterministic, an approach that calculates the cost elements and the total cost based on discrete values. Generally, these represent the most likely values and the probability is not directly embedded in the assessment

Techniques: Sensitivity Analysis, Cost Growth Factors and Historical Analogies, these all use discrete inputs to generate a single output

o The Probabilistic approach includes the Probability theories to calculate the cost uncertainties

Techniques: Propagation of Errors, Monte Carlo simulation, Expert judgement, Error of Estimating Method, Method of Moments aim to produce a Probability Distribution Function or a Cumulative Distribution Function.

The yellow colour columns require the evaluator to input information concerning:

- Distribution Type – discrete or continuous probability distributions are required here. As a guide to the user on the correct choice, the spread-sheet (included in the same Excel file) provides a detailed description of the possible continuous distributions

- Estimate Uncertainty Range (σ) – when the user knows, the range of variation of the cost element should be entered. If it is not possible to input a range, the worst and the best ranges should be included

- Cost impacts (3 points estimate):

o Best case – represents the best scenario of the cost distribution

o Most Likely (µ) – this is also called Mode of the distribution, or simply the value that happens more often in a set of data

o Worst Case - represents the worst scenario of the cost distribution considered

The green columns represent the actual scoring mechanism. A score value for each of the Uncertainty cost values is required:

Uncertainty Impact (shown in Figure 13) – Low Impact (25% of the total impact), Medium (50%) and High (100%)

Figure 13 Uncertainty Impact

Partial Scores (%) - the score choice on the previous cell (Uncertainty Impact) has to be entered here in the form of percentage. Three values are available: 25% for the Low score, 50% for the Medium and 100% for the High score;

The column in red, it is automatically calculated:

- Total Score (%) – this calculates the mere arithmetic average between the partial scores of the cost element Uncertainties

- Adjusted Uncertainty Range (σ) – the ‘Estimate Uncertainty Range (σ)’ entered earlier will be modified according to the ‘Total Score (%)’ index. When the ‘Total Score (%)’ will be lower than 50% the old range will be reduced, while if the ‘Total Score (%)’ will be larger than 50% the ‘Estimate

Uncertainty Range (σ)’ will be more widely adjusted. However, if the ‘Total Score (%)’ equals to 50% will result an unchanged ‘Estimate Uncertainty Range (σ)’ (approach validated in section 4.2);

Finally, there is a requirement to enter:

- Comments/Notes – a record of information that is essential for further refinement.

4.5 Monte Carlo Simulation

The Monte Carlo Simulation in this project aims to elaborate the information input by the user into the Scoring Mechanism and return a new function of cost

The spread-sheet here considered wants to be strictly connected with the Scoring Mechanism one. This is because, the information input in the card by the User needs to be transfer in the Simulation sheet, in order to gain the elaboration wanted.

Consequently, the Most Likely (µ) and the Adjusted Uncertainty Range (σ) of each cost element will be copied in the Simulation sheet.

This data together with the cost function, preliminary sets by the User, and a grill of random numbers for the different cost elements, provide the estimator with a new reshaped cost distribution.

It is worthwhile mentioning that in this project, the Monte Carlo Simulation, do not represents the core part of the development, but just a fairly simple technique to obtain a quick visual evidence of how the cost function can be readjusted.

Consequently, in order to simplify the study, three different type of distributions (Triangular, Uniform and Gaussian) were analysed for each of the three cost elements take into account.

For each of these, a set of input were found in the web to shape the distribution samples. As briefly shown in Figure 15 the inputs can vary from a range of ±3 with a total number iteration equal to 2000, average (µ) equals 0 and sigma (σ) equals 1: Figure 14 Three distributions (Triangular in green, Uniform in blue, Gaussian in red) -50 0 50 100 150 200 250 -4 -3 -2 -1 0 1 2 3 4

Figure 15 Distributions Input

A good enough quantity of random numbers (according to the Law of large numbers) were then taken into account to provide, the preliminary set function

For each of the set scenarios, with three random numbers for each type of distributions, as shown in Figure 16 the cost function is calculated (y).

Figure 16 Monte Carlo Simulation

Statistics about the minimum value, the maximum value, the average, the sigma and the variance are extrapolated from the different random scenarios.

Afterwards, the range of output is subdivided in ten section and each result will be then allocate to their own one (Figure 16).

These data will simply allow to shape the new reshaped distribution of cost, as shown in Figure 17.

4.6 The Framework Logic

To better understand the Framework logic, a flowchart is provided in Figure 18, and a case study is provided in section 4.1.

0 50 100 150 200 250 300 350 400 0 2000 4000 6000 8000 10000 £

Disposal Cost

The Framework logic step-by-step:

Preparation Phase:

The user needs to gather all information about the Disposal Cost structure for the product(s) considered and the ROU Register needs to be populated and prepared for the assessment;

Scoring Card compilation:

The User has to identify the top Uncertainties, which affect the cost elements considered;

In this phase the evaluator can use the ROU Register in order to better identify the top Uncertainties;

Information regarding the type of assessment is required to be entered: Is it

Deterministic or Probabilistic?;

The evaluator needs to define the type of cost distribution considered. The choice is supported by the Distributions sheet embedded in the Framework; At this stage, the three point estimate has to be entered to defined the μ and

the σ of the cost distribution;

For each of the Uncertainties identified, there needs to be score entered using the Low-Medium-High card. The new adjustment σ will be automatically calculated;

A Monte Carlo simulation will be performed according to, the μ, the adjusted

based on σ, and the cost function defined. The outputs will show the Most

Likely Cost of Disposal and its intrinsic Variance.

4.7 Summary

In this section is shown how the Framework was developed. Step by step is explained how the different part of tool born and how they were make cooperate together.

5 RESULTS

5.1 Introduction

As earlier mentioned in the Section 3, one of the project intent has been the identification of best practices for the product end-of-life treatment.

The survey undertaken (Section 3.1) highlighted the following information (Figure 19):

The results obtained clearly highlight that Uncertainties and Risks are the major defects of inaccuracy for the Disposal costs estimations. This is because, companies do not feel necessary or profitable to investigate the in detail the cost aspects for the last stage of the CADMID.

This drives a poor sophistication on the evaluation of those costs, and moreover standards for the industries seems to lack in guidance information.

Afterwards, the commonalities between different industries have been identified and then summarised in a mind map: IDEF (Integrated Computer-Aided Manufacturing DEFinition).

The IDEF is a standard modelling representations for company architectures. In this case, an IDEF has been drawn to understand each step of the Disposal process. It aims to represent every single process, imagining those as single “black box” where input/s are transformed through the process into output/s. Every process can be deployed from a macro level (Level 0) to a micro one (Level 2), as a top-down approach.

The IDEF is an interesting instrument to better understand the process and to catch the disposal requirements (inputs of the “black boxes”, the constraints (interrelation between the “black boxes” and the product end-of-life options (output of the processes)) (Figure 20):

Concurrently to the disposal modelling, through interaction with the industrial contacts (mainly from Air Systems, department of Defence companies), it has been deducted that the current cost evaluation for disposal is nowadays one of the main challenges in defence industry, especially for project with UAVs.

The reason is because the current budget dedicated to the final stage of the CADMID represents a very low percentage of the total provided.

An example of a military aircraft F-35 has been taken into account to demonstrate that the disposal costs are insignificant compare to the Operating costs (44% for a military aircraft F-35) or the Acquisition one (18% of the total LCC) (Figure 21) [16].

Because of the narrow margin on this activity, it is not justify an accurate and deep analysis of the cost of disposal its uncertainties.

boar

The work identified that an analysis of the uncertainty and the risk is necessary when they are negative or positively disturbing the total LCC. In the case study considered before, the disposal cost represents 43,000,000 Canadian $, where

(almost 0%), even if it affects by a high uncertainty of 100%, will represent a negligible deviation on the total life cycle cost (0.1%).

The study carried out needs to relate to all those projects in which the disposal represents a higher slice on the LCC pie. Such as the case of vehicles, which can embed hazardous material, or the case of the disposal of a nuclear facility (military or power plants) or the case of cleaning up of unexploded ordnance.

However the industry interactions evidence that defence companies have several projects with a requirement to understand the cost of disposal. Because disposal represents a new requirement, they have to now address it for legacy projects and potential new ones.

It is worthwhile mentioning, that these long life projects are essentially affected by cash flow issues as to dispose a military system the contract needs to be agreed several years before the actual moment of happening.

5.2 Case Study

To verify the conceived tool, a simulation, of how industry should make use of it, has been carried out.

Firstly, it is necessary to describe what the Framework structure is, the logic and its conditions of operability.

Moreover it is an instrument, which aims to support the evaluation of the costs for projects which are platforms which have been in use for many years, at the early stage of the CADMID, such as the early product design and development or later stages before the Disposal one.

The Framework will assist the evaluator to include uncertainties in the costs of disposal, so to improve the current lack of carelessness during the evaluation. Because of the tool complexity, it needs to be used by an expert in disposal or an engineer, or possibly a team of experts in cost evaluation.

It is worthwhile noticing, that the simulation undertaken has been using subjective data, as the availability of information was influenced by the confidentiality constraints, which affects the Defence industry. Consequentially, a hypothetical case study have been created which has then been validated by experts engineers.

The simulation carried out aims to follow the process of evaluation step-by-step and to, then, summarised the tool usage in form of a list of processing steps.

The evaluator will, firstly, need to gather information regarding the costs of disposal for the product or project considered. This information is the result of in-depth process of cost analysis, which mainly considered two different sources of information:

- Air platform – it represents a part of the Line-Replaceable Units (LRUs) in the Defence, and it is the analogue of the Bill of Material (BoM) for any other product. In other words, it denotes the ordered list of how materials and components are interrelated together and how they will be processed during the disassembly or dismalting;

- Risks, Opportunities and Uncertainties Register – this is the structured database, earlier analysed, of information about Risks, Opportunities and Uncertainties cost related. Shown in Figure 8.

The register will provide the evaluator with the awareness needed to better embed the uncertainty in the costs assessment.

The user is, then, asked to compile the scoring mechanism, which aims to return a readjusted and more truthful shape of the distribution cost under uncertainty.

As shown in Figure 22, the user will gather the data necessary to refill the card from the left to the right:

Figure 22 Example of scoring mechanism compiled

1. Each of the cost elements identified from the Air platform has to be analysed separately and they will represent the subject of the further investigation. In the example, the cost of the Labour (in £) and the cost of the Composite

Material (in £) are taken into account.

2. For each of the cost elements the User is asked to research the top uncertainties involved.

This process is guided by the information contained in the ROU Register (shown in Figure 9).

Each of the uncertainties identified will be registered in the scoring card with their respective Identification (‘ID’ in the card) number (as Shown in Figure 22, second column from the left called Uncertainties involved (ID)). In the case study carried out, for the voice Labour Cost (£) there were three top uncertainties (ROU Register ID: 101, 57, 82) influencing the cost element.

3. The user is, then, required to input the whether the evaluation process will be Deterministic or Probabilistic.

As earlier explained, the Deterministic approach make use of discrete and exact data without taking into account the cost uncertainties and risks related.

The Probabilistic approach, instead, is including the uncertainty according to the probability theories.

![Figure 2 Product value gain [6]](https://thumb-eu.123doks.com/thumbv2/123dokorg/7624907.116628/13.893.152.746.497.783/figure-product-value-gain.webp)

![Table 1 Factors affecting the product disassembly [3]](https://thumb-eu.123doks.com/thumbv2/123dokorg/7624907.116628/24.893.127.768.172.532/table-factors-affecting-product-disassembly.webp)