DIPARTIMENTO DI ECONOMIA E MANAGEMENT

Corso di Laurea in Strategia, Management e Controllo

TESI di LAUREA

“Employees' Corporate Social Responsibility policies and

Corporate Strategy. A comparative analysis between

Italian and Portuguese companies”

Relatore: Candidato:

Prof. Antonio Corvino Grazia Ferrò

1

Index

Ringraziamenti………...3

Introduction………5

1. Corporate Social Responsibility in the literature………..8

1.1 Evolution of the concept of Corporate Social Responsibility………...8

1.2 Stages of development of CSR into the corporate strategy………..14

1.3 Studies that converge into CSR………...17

1.3.1 Stakeholder approaches to CSR………...17

1.3.2 Studies on Business Ethics………..22

1.4 Resource-based view of the firm and human capital……….25

1.4.1 RBV and intangibles………27

1.4.2 Human resource: value and management………31

2. Communicate and evaluate CSR’s effects………...36

2.1 Communicate with employees……….36

2.1.1 Evidence and tools of communication……….43

2.1.1.1 Code of conduct………...45

2.1.1.2 Social Balance……….49

2.1.1.3 Specific Standard of conduct: SA8000 and OHSAS 18001……….53

2.1.1.4 House organ………59

2.1.1.5 Focus group……….61

2.2 Evaluate CSR’s effects on the performance……….63

2.2.1 The Balance Scorecard (BSC)………..65

2.2.2 The Social Statement………66

3. Two business cases: the Portuguese Somague and the Italian Astaldi……….69

3.1 Introduction………..69

3.2 Somague………...69

3.2.1 History, Business Areas and Mission………...69

3.2.2 Code of Ethic and Conduct………...71

3.2.3 Economic data from consolidated annual reports of 2009-2013………73

3.2.4 Non-economic effects of employees’ policies from 2009 to 2013………75

3.3 Astaldi Group………..79

3.3.1 History, Business Areas and Mission……….79

3.3.2 The Code of conduct………81

3.3.3 Data from consolidated annual reports of 2009-2013………...83

3.3.4 Non-economic effects of employees’ policies from 2009 to 2013……….85

2

3.4.1 Convergences and divergences: the causes of the main variations……….89

3.4.2 A comparison between companies’ non-economic profile………93

3.4.3 The correspondence of the Codes of Ethic to the standards………..95

Conclusions………..98

3

Ringraziamenti

Vorrei dire grazie alle persone che hanno reso possibile la stesura del lavoro e a quelle che mi hanno accompagnata nell’avventura universitaria durante gli ultimi due anni a Pisa.

Ringrazio innanzitutto il Professore Antonio Corvino, relatore della mia tesi e professionista serio, attento e sempre disponibile ad accogliere idee ed opinioni dei suoi studenti, che ha accolto con entusiasmo la mia proposta di collaborazione per realizzare la tesi di laurea all’estero. Ringrazio anche il Professore Arnaldo Coelho, che all’Università di Coimbra, durante la mia esperienza Erasmus, mi ha aiutato nella prima fase di individuazione e impostazione del lavoro di tesi.

Ringrazio la mia famiglia: mio padre, che mi ha incoraggiato nei momenti di indecisione e di sconforto, non mi ha fatto mai mancare il famoso “in bocca al lupo” prima di un esame e mi ha sempre ricordato con rigore che “quando si studia per un esame non esistono feste, né domeniche o gite fuori porta”; mia madre, che si è sempre preoccupata di non farmi mancare nulla, che mi ha quasi viziata con l’unico scopo di garantirmi un benessere tale da permettere che tutte le mie energie si concentrassero nello studio, che mi ha sempre messo davanti ai miei doveri con severità e che aspettava con ansia e dolcezza, dopo mesi, i miei rientri a casa; mio fratello, che, pur serio e innamorato di ogni forma di cultura, preferisce non prendermi mai troppo sul serio, nemmeno a 24 anni compiuti, e rispetta il mio mondo un po’ più superficiale; mia sorella, che ha convissuto pazientemente insieme a me nei primi difficili anni universitari e che, per scelte lavorative, non può festeggiare con noi un giorno così importante, ma l’orgoglio di cui ci riempie con i suoi successi sin da sempre allevierà anche questo dispiacere.

Ringrazio tutti i parenti per essere presenti, affettuosi e attenti, per essersi sempre interessati alla mia carriera universitaria, e per avermi trasmesso il senso di famiglia unica e coesa ma anche per avermi dato l’esempio, con i loro successi, facendomi credere che solo facendo dei sacrifici si raggiungono importanti traguardi; in particolare ringrazio anche cugine e cugini, amici e complici di momenti divertenti e spensierati. Un bacio affettuoso va a quelli che non ci sono da anni, che ci mancano, ci proteggono e ci guidano.

Ringrazio Ivano, con cui ho condiviso tutta la mia vita negli ultimi cinque anni e che è stato un collega universitario incomparabile a qualsiasi altro, riprendendo i miei momenti di svogliatezza, trasmettendomi diligenza e pazienza; ha condiviso con me lo studio, le ansie, le gioie, la vita di ogni giorno, con gratuità e dolcezza, donandomi con preziosità la possibilità di entrare e restare nel suo mondo.

Ringrazio gli amici che ho accanto da sempre, che sono cresciuti insieme a me, che sin dai tempi dei banchi di scuola mi hanno fatta ridere di gusto e non hanno mai vissuto l’ambiente circostante con competizione, e che ora, nonostante la distanza fisica continuano a esserci ogni

4

giorno con un messaggio o una telefonata per continuare a condividere tutto con me: siete speciali!

Ringrazio la famiglia Romeo: Andrea e Michela, amici di infanzia inseparabili, nonostante città e percorsi diversi una volta lasciato il paese; Luisa e Cosimo, che mi hanno sempre fatta sentire una di famiglia e hanno tenuto compagnia ai miei genitori, specialmente durante momenti di nostalgia quando tutti noi ragazzi eravamo lontani.

Ringrazio le mie coinquiline Alessandra, Oriella e Rosita, per avermi accolta nella loro convivenza, per aver sopportato tutti i miei stati d’animo e le mie esigenze, per avermi regalato momenti di sollievo, spensieratezza e divertimento, per avermi insegnato quale fosse la vera vita universitaria. Sempre disponibili e sensibili.

Ringrazio Maria e Giulia, che dopo aver passato insieme a me i primi tre anni universitari mi sono rimaste accanto, non mi hanno mai fatta sentire “indietro” e mi hanno sempre incoraggiata a far meglio con la loro carica e la loro positività.

Ringrazio tutte le persone che ho avuto la possibilità di frequentare negli ultimi anni a Pisa, con cui ho trascorso momenti di svago, giornate e serate interminabili, e che oggi sono qui insieme a me per festeggiare. Ma ringrazio anche tutti i ragazzi con cui condivido i miei brevi periodi di vacanza a casa e che oggi non ci son potuti essere: grazie per avermi sempre accolta, nonostante il mio andirivieni.

Ringrazio anche i ragazzi che ho conosciuto in Erasmus: Margaret, Honza, Marlena, Lay, Michael, Katerina, Roberto e Chiara. Anche in Portogallo non sono mancate persone speciali, con cui ho potuto confrontarmi e a cui mi sono affezionata con sincerità.

Ringrazio infine le persone con cui ho condiviso la mia quotidianità in questi anni e che hanno rappresentato una seconda famiglia: Vincenzo, Peppe e Raissa. Un dottorino di tutto rispetto, sensibile e sincero, che prende lo studio con molta serietà, che mi ha permesso di instaurare con lui un rapporto confidenziale e che mi ha tenuto compagnia con la sua ironia e la sua forza. Un bonaccione di amico, con cui ho un rapporto unico di odi et amo, che trasmette spensieratezza e positività, ti fa divertire e, disponibile in qualsiasi momento, trova sempre una soluzione ai tuoi problemi. Una piccola bomba di energia e di guai, la sorpresa più grande di questi ultimi due anni: una persona che ho scoperto essere unica, sincera, affettuosa, schietta, in grado di darmi spensieratezza e serenità smorzando i miei inutili momenti di serietà e che non ha bisogno che tu sia fisicamente vicina per farti sentire il suo calore; un’amica che tiene a mente ogni mia cosa come fosse la sua, con cui è facile confidarsi senza timore di giudizi, che comprende tutti i miei stati d’animo e che ormai fa parte dei miei affetti più cari.

Tutti avete contribuito a farmi raggiungere questo traguardo, trasmettendomi forza, positività, ottimismo, fiducia in me stessa, rispetto per il lavoro degli altri. Grazie di cuore.

5

Introduction

To be a Socially Responsible company: the complex of the business choices pays management’s attention to a combination of different problems, questions, doubts, responsibilities, which could causes the conception of priorities or preferences on the system of values that may cause the reduction of relevance of being socially responsible.

The aim of the thesis is to verify if the Corporate Strategy of a company could benefit from its Corporate Social Responsibility (CSR) and how these two basics are integrated. I will try to explain what does being socially responsible mean, why a company should be responsible, in regard to whom and in which way, and finally which are the most appropriate practices to result into a Socially Responsible Company. The CSR generally concerns the ethical implications into the strategic vision of the firm, but also the effective management of social and ethical policies that the company observes in its business activities. Most of the times it is interpreted as oriented to customers, as, for instance, policies about renewable energy or diffusion of organic products, assistance system and customization of the products; the focus of the thesis is about CSR oriented to the employees, as a class of company’s stakeholders, with their expectations and their value. The goal is to explain how CSR’s policies on employees could integrate the Corporate Strategy and generate added value, improve strategic power and increase the competitiveness of the firm.

First of all, as many definitions as possible of the Corporate Social Responsibility from the literature are listed and then, analyzing all the linked topic about the employees, the study shows how the firm can communicate and evaluate these policies. At the end of the thesis two business cases are reported, in order to show the results of a qualitative analysis on the phenomenon of Corporate Social Responsibility into two companies coming from different geographical and political contexts.

In the chapter 1, I report the evolution of the concept of Corporate Social Responsibility, analyzing studies from every decade from the 50s to nowadays and mentioning authors as H. R. Bowen, W. Frederick, Davis and McGuire, M. Friedman, the Corporate Social Performance Models of A. B. Carroll, S. L. Wartick and P. L. Cochran, J. D. Wood and Carroll and Schwartz again in 2003, when the CSR’s influence spheres became 3: economic, legal and ethical. After a description of the stages of development of CSR into corporate strategy (informal, current, systematic, innovative, dominant), there is the description of two studies that converge into CSR: a) the stakeholder approach, using the main classification as internal and external or primary and secondary, analyzing the Freeman’s work Strategic Management: A Stakeholder

Approach; b) the Business Ethics, mentioning briefly the American Federal Government

6

compelling organizations to create ethical standards. After a description of the Resource Based View and of intangible as human capital, an in-depth analysis moved from concepts of skills, competencies, experiences, knowledge, attitudes, intellectual capital, to the added value of the human resources (HR). In this section I explain the importance of human resources as a strategic resource: a good management of the HR allows to attract and hold employees who are qualified and motivated for good performance, ensuring organizational and behavioral flexibility. The satisfaction of their needs through CSR’s policies allows indirectly to realize a better work environment, produce higher performance, improve company’s reputation, attain a position of competitive advantage.

In the chapter 2, the communication of policies and the evaluation of the Corporate Social Responsibility’s effects are analyzed. The communication of the policies is important in order to diffuse them among the stakeholders and to create a set of ethical rules, but while the communication of the policies’ effects allows employees to understand which is their contribute to the value of the firm. There are a lot of ways and tools of communication and the choice depends on a lot of parameters as the possibility of reply, the target, the addressees, the resources and capabilities of the sender. Moreover, every tools of communication has its own characteristics: formal and complicated or quickly and clear. It is important to test the effectiveness of the communication through review or audit using interview, employees focus group, surveys, but also to verify the clarity and timeliness of message, review frequency of meetings, understand the employees’ need: it is manager’s responsibility to avoid misunderstanding in communication and the European Guide recommendations on CSR’s communication are listed. The Code of Conduct, Social Balance, International Standards as SA8000 and OHSAS18001, House organ and Focus Group are analyzed as tool of communication: for each one I describe why to choose it, how to use it, characteristics, basics principles, possible effects. Then, the tools for a right evaluation of effects of CSR’s policies on employees are the Balance Scorecard and the Social Statement: the first one, focusing especially on the innovation & learning perspective, is useful to explain how the firm can manage and measure the workers’ ability to improve and adapt to changes of the business, while the second one is an Italian Governmental tool that shows a set of simple and flexible CSR performance indicators and support the control of results in space and time.

In the chapter 3, two business cases are described: the Portuguese Somague and the Italian Astaldi, both working in the sector of construction and concessions. I chose this business because I think it is so full of risks and continuous changes that configures itself as a really sensitive sector to CSR’s policies addressed to employees. The choice of the Portugal derives from my Erasmus experience of last semester: I had the opportunity to check information about the company thanks to the Professor Arnaldo Coelho who helped me at the beginning of my work. The main important economic data, as income, EBIT, invested capital, shareholders’

7

equity, ROI, ROE, ROS, the basics of the Codes of Conduct and non-economic effects of CSR’s policies in each company are listed, explaining and comparing the trend of the companies, highlighting which policies they adopt every year also on the basis of the economic and political context and which is the reaction of the staff. At the end, there is a comparative qualitative analysis that shows convergences and divergences within companies, their probable causes and permits to deduce the study’s evidences.

From a methodological point of view, I have consulted the electronic databases provided by the library of Universidade de Coimbra, as B-on or Proquest or ABI-INFORM Global, in order to search papers from scientific Journals; I have also consulted all the books and papers that Professor Antonio Corvino has kindly proposed and any books from the educational matter during the required course at University of Pisa. For the last chapter, I have consulted the Consolidated Annual Reports of both companies since 2009 to 2013, their Codes of Conduct and I have elaborated all the tables that needed for a clearer exposition and comparison of the cases, always using official data.

8

1. Corporate Social Responsibility in the literature

1.1 Evolution of the concept of Corporate Social Responsibility

The world of business literature started to talk about Corporate Social Responsibility (CSR) since 1950s because of the emerging problems on business and society worlds that could be associated with this concept. During these years the concept of CSR changed continuously, each time taking a different connotation and enlarging its dimension; it has been transformed from a doubtful idea to a high-ranking topic on research studies1. It also evolved into two aspects: a) the level of the analysis moved from a discussion of its macro social effects to its impact on organizational processes and performance; b) researches shifted from explicitly normative and ethics-oriented argument to implicitly normative and performance-oriented studies2. In this paragraph we are going to explore the literature review on CSR and its dimensions along the time, but it’s necessary to underline that right now there isn’t yet only one accepted definition of CSR, even if most of the researches accept CSR like the combination between socially responsible involvement and the business’ objectives3

, because this combination makes CSR to be seen as a strategic approach.

The 1950s and 1960s:

In Bowen’s book Social Responsibilities of the Businessman (1953) firms are the central point of the power and have great impact on the lives of people; CSR is seen as a guide that must educate business and about the social responsibility of businessmen it declaims: “it refers to the obligations of businessmen to pursue those policies, to make those decision, or to follow those lines of action which are desirable in terms of the objectives and values of our society”4. In 1954 P. Drucker follows the same ethical obligation argument of Bowen and asserted that “CSR has to consider whether the action is likely to promote the public good, to advance the basic beliefs of our society, to contribute to its stability, strength and harmony”5.

In 1960s the CSR literature focused more on what CSR actually meant and how much is important in business and society; in these years a lot of books and paper have been published from different authors that concentrated on different themes (social purposes, responsibilities, shareholders, social system), thus beginning to come out all the aspect of CSR that will be detailed later. William Frederick asserted that “CSR implies a public posture toward society’s

1 Mc Williams, A., & Siegel, D. S., & Wright, P. M. (2006), “Corporate Social Responsibility: Strategic Implications”, Journal of Management Studies, Vol. 43, Issue 1, pp. 1-18

2

Lee, M-D. P. (March 2008), “A review of the theories of corporate social responsibility: Its evolutionary path and

the road ahead”, International Journal Management Reviews, Vol. 10, Issue 1, pp. 53-73 3

Kotler, P., & Lee, N. (2008), “Corporate Social Responsibility: doing the most good for your company and your

cause”, John Wiley & Sons Inc., Hoboken, New Jersey, pp. 9-10 4

Bowen, H. R. (1953), “Social responsibilities of the businessman”, New York, Harper, p.6

5

9

economic and human resources and a willingness to see that those resources are used for broad social ends and not simply for the narrowly circumscribed interests of private persons and firms”6

. Davis and McGuire focused on the concept of responsibility, sustaining that social responsibility implies that companies assume responsibilities beyond their economic and legal obligations7 and that if social responsibility and power would be relatively equal, then involvement in social responsibility activities would lead to the gradual erosion of social power. Davis first sustained the social responsibility as a part of management context and emphasized that it is related to the “business decisions and actions that are undertaken for reasons at least partly outside the scope of direct economic or technical interests company” and “some socially responsible business decisions can be in the long-term, complex process of analysis are explained as a good time for the company long-term economic effect”8. Milton Friedman, considering the forces of capitalism affirmed the opposite of McGuire, writing that “few trends would so thoroughly undermine the very foundations of our free society as the acceptance by corporate officials of a social responsibility other than to make as much money for their shareholders as they possibly can”9

and also Davis some years later changed his concept of responsibility highlighting that business does not exist alone and that an healthy business cannot exist within a sick society, since there is mutual dependence between business and society10. In the end of 1960s, thanks to Heald, authors began to talk about business practices around the area of social responsibilities including topics like philanthropy, customer relations, employee improvements and stockholder relations.

At last, following more recent critics moved from Carroll and Frederick, we could say what CSR meant in 1950s: the idea of corporate managers as public trustees, the idea of balancing competing claims to corporate resources and the acceptance of philanthropy as a manifestation of business’s support of good causes.

The 1970s and 1980s:

In this two decades we start to talk again about Friedman that reinforced his work accepting free market rules, social demand in the company and laws and ethical customs in CSR; the author sustained that social actions are acceptable if they are justified from firm’s interest and wrote that “there is only one responsibility of a company, namely to use its resources and engage in activities designed to increase its profits, as long as it respects the rules of the game, or rather, as

6 Frederick, W. C. (1960),“The growing concern over business responsibility”, California Management Review,

Issue 2, p.60

7

McGuire, J. W. (1963) “Business and Society”, McGrawHill

8

Davis, K.(1960), “Can Business Afford to ignore social Responsibilities?”, California Management Review, Vol.2, pp.70-76

9

Friedman, M. (1962), “Capitalism and Freedom”, Chicago University Press, p.133

10

Davis, K. (1967), “Understanding the social responsibility puzzle: what does the businessmen owe to society?”, Business Horizons, Vol.10, pp. 45-50

10

long as it engages in an open and free competition without deception and fraud”11

. Considering competition of the market, Davis sustained also that if a firm does not use its social power it will lose its position in society because other groups will occupy it assuming those responsibilities12. Two years later Davis and Blomstrom defined orientation of CSR as “the responsibility of decision-makers, to take actions will not only meet their own interests, but also to the protection and enhancement of public wealth”13

. Moreover, during these years the focus was on processes of CSR that are not in conflict with interests of business: Ackerman, Fitch and Sethi wrote about internal structure, management of social issues and solving social problem related to organization of the firms14. The apex of these studies arrived with Carroll, who developed a framework and conceptual model of corporate social performance to explain thoughts on CSR and offered the definition: “the social responsibility of business encompasses the economic, legal, ethical and discretionary expectations that society has of organizations at a given point in time”15

(in 2003 Schwartz transformed the model into “three model of CSR” considering only economic, legal and ethical areas). The model will be developed by Wartick and Cochran (1985), and Wood (1991):

Carroll’s model16

:

CSR is like a four-level pyramid that corresponds to four dimensions: economic, legal, ethical, philanthropic. The base is represented by economic responsibilities like maximizing profits and market share actions, maintaining a strong competitive position or maintaining high level of efficiency; the assumption is that the other three components can be built only on a solid and profitable base. The legal dimensions reflect the imperative for the company to obey the laws and the regulations of local and regional governments and authorities, in order to fulfill the relation between company and society. The level of company’s ethical responsibilities refers to those activities which are not prohibited by law but are expected by the society members: standard, norms, respect of the moral rights of the stakeholders. The activities of the top area, discretionary responsibilities, include those that reflect company’s

11 Friedman, M. (13 September 1970), “The social responsibility of business is to increase its profits”, New York

Times

12

Davis, K. (1973), “The case for and against business assumption of Social Responsibilities”, Academy of Management Journal, Vol. 16, NO. 2, pp. 312-322

13

Davis, K., & Blomstrom, R. L. (1975), “Business and Society: environment and responsibility”, McGrawHill, 3rd ed

14 Ackerman, R. W. (1973), “How Companies respond to Social Demands”, Harvard Business Review, pp. 88-98;

Fitch, H. G. (1976), “Achieving corporate social responsibility”, Academy of Management Review, Vol.1, pp. 38-46; Sethi, S. P. (1975 spring), “Dimensions of corporate social performance: an analytic framework”, California Management Review, pp.58-64

15

Carroll, A. B. (1979), “A three dimensional conceptual model of corporate performance”, Academy of Management Review, Vol.4, p.500

16

Carroll, A. B. (1991), “The pyramid of Corporate Social Responsibility: Toward the Moral Management of

11

implication into programs that promote human welfare: financial contribution in arts, education, sports and community. If company does not participate to these humanitarian programs it’s not considered as unethical because these actions require voluntarism and this is the main difference between discretionary and ethical areas. Examples of voluntary activities during the time in which the paper was written are “conducting in-house programs for drug abusers, training the hard-core unemployed or providing day-care centers for working mothers” (Carroll, 1979, p.500). The logic of Carroll’s pyramid respects the principles of Maslow’s pyramid of needs: if the basic component, the economic, is not satisfied, then cannot access the other components.

Figure 1.1: Carroll’s CSR pyramid.

Source: The World Business Council for Sustainable Development (Making Good Business Sense). Diagram of Carroll’s CSR Pyramid. Carroll 1991.

Wartick and Cochran’s revisitation17

:

in 1985 Wartick and Cochran reinvented the Carroll’s corporate social performance model extending the three dimensional integration of CSR, social responsiveness, and social issues; the first should be thought as a principle, the second as a process and the third should be thought of as a policy. They emphasized also that Corporate Social Performance can integrate the three dominant orientations in the field of business and society18: a) the philosophical orientation (related primarily to the principles of social responsibility); b) the institutional orientation (related primarily to the process of social responsiveness); c) the organizational orientation (related primarily to the policies of social issues management).

17

Wartick, S. L., & Cochran, P. L., (1985),“The evolution of the corporate social performance model”, Academy of Management Review, Vol. 10, pp. 758-769

18

Moura-Leite, R. C., & Padgett, R. C., (2011), “Historical background of corporate social responsibility”, Social Responsibility Journal, Vol. 7, NO 4, pp.528-539

12 Wood’s work19

:

The author reinvented the corporate social performance model and based it on three main principles: first she showed the relation between Carroll’s principle of CSR (economic, legal, ethic and discretionary) with CSR principles of social legitimacy, public responsibility and managerial discretion; second she identified processes of social responsiveness that embraced more aspects than Carroll’s like environmental assessment, stakeholder management and issues management; third she created a new category on corporate behavior. The model proposed by Wood is more comprehensive than Carroll’s, since firms and their performance were viewed as locus of actions that have consequences for stakeholders and society as well as for themselves20.

Since this moment firms became more responsive to their stakeholder: authors like Preston and Post tried to better explain that firms should consider the consequences of their action but are not required to resolve all the problems of the society, they should only target areas related to their interests and activities; the authors also wrote that it’s difficult to define what is public or what is private but social action could be justifiable if provide benefit to the public. In 1984 thanks to Drucker and the review of his 1954 work, authors started to talk about profitability in order to understand the relationship between business and society, asserting that CSR could be an opportunity for businesses because can improve financial profitability. Moreover, in the same year Freeman conceived the stakeholder theory of the firm, recognized the growing importance of ethics and believed that corporate performance was affected not only by firm’s shareholders but also by its stakeholders such as employees, customers and governments; this theory is used as a basis to analyze groups to whom the firm should be responsible.

The 1990s and forward:

As we have already shown, during 1990s one of the most important literature contribution on CSR was by D. J. Wood. In the mid-1990s the growing importance of intangible assets (such as goodwill, reputation, human capital) and the changing relationship between business and society brought a lot of researches to adopt the stakeholder theory. In fact the corporate perspective of stakeholder theory describes specific corporate characteristics and behaviors regarding stakeholders, identifies “the connection, or lack of connections, between stakeholder management and achievement of traditional corporate objectives”, “interprets the function of the corporation, including the identification of moral or philosophical guidelines for the

19

Wood, D. J., (1991),“Corporate social performance revisited”, Academy of Management Review, Vol.16, pp. 691-718

20

Wood, D. J., (2010), “Measuring corporate social performance: a review”, International Journal of Management Review, Vol. 12, pp. 51-84

13 operation and management of corporations”21

. Clarkson also underlined the necessity to separate stakeholder issues from social issues because social issues often prompt legislation or regulation, but if no such legislation exists it may be a stakeholder issue and not necessarily a social issue22.

In 2003 Carroll and Schwartz23 revisited the Carroll’s CSR pyramid but the latter author sustained that only three areas are strategic (economic, legal and ethical) because the philanthropic one could be subject to inappropriate definition or to confusion with the ethical one; he also believed that pyramid may induce the idea of hierarchy and the philanthropy area may give the impression that it is the most important component of the model. In fact, while a lot of authors that use pyramidal model consider the top the most important part, on the other hand Carroll considers the basis the most important part; therefore, the use of the pyramid could generate wrong interpretation. Moreover, in Schwartz opinion, pyramid can not capture the link between social responsibility dimensions; so, the three dimensions considered by the author are addressed in a more complex manner, using the Venn diagram in order to avoid idea of hierarchy and to highlight the link between the three spheres (Figure 2). The economic sphere includes activities that have economic (directly and indirectly) impact on the company, for example those that refer to profit maximization and market share increase or those that refer to moral actions of employees’ increase and company image improve. The legal sphere includes company’s activities under legal regulations: the term of legality includes compliance with legal regulations, dispute avoidance and law anticipation. The ethical sphere includes actions expected by society and responsiveness both to domestic and global imperatives; activities are considered outside of this sphere if they are immoral by nature or are intended only to produce net profit for the company and not for the stakeholders. It is hard to believe that company could take actions that are only economic, only legal or only ethical; even if spheres interfere only in some areas, the author believes that there will always be an overlap between the three spheres up to a certain point24.

From 1990s until now, also international organizations (The United Nations, the World Bank, the Organization for Economic Co-operation and Development, the International Labor Organization) have supported the movement research about CSR: for example, during World Economic Forum in Davos in 1999, UN Secretary General Kofi Annan hailed a draft agreement to comply with the World leading international corporations social responsibility that included principles of CSR: human rights, standards of work (abolition of forced labor, elimination of

21 Donaldson, T., & Preston, L. E., (1995) “The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications”, Academy of Management Review, pp. 65-91

22

Clarkson, M., (1995), “A Stakeholder Framework for Analyzing and Evaluating Corporate Social Performance”, Academy of Management Review, pp. 92-117

23

Schwartz, M. S., & Carroll, A. B., (2003), “Corporate Social Responsibility: a three domain approach”, Business Ethics Quarterly, 13(4), pp. 503-530

24

Mihalache, S. S. (2013), “Aspects regarding corporate social responsibility definition and dimensions”, International Conference “Marketing-from information to decision”, 6th

14

child labor, abolition of all forms of discrimination in employment), ecology, anti-corruption, legal responsibilities, global responsibility (implies voluntary compliance with international standards of social responsibility), environmental responsibility, cultural and ethical responsibility, philanthropic responsibility. In 2011 the European Commission gave in the European strategy for 2011-2014 a new definition of CSR as “the companies’ responsibility for the impact they have on the society”.

Figure 1.2: Schwartz’s CSR influence spheres. Adapted from Schwartz and Carroll (2003).

Source: wordpress.com; ICTs for development.

Finally, during the years concept of CSR changed a lot of times, included new parameters and new approaches to management of human capital and stakeholder engagement, interesting researches, NGOs, international organization and obviously firms (table 1). Definition of CSR differs from one author to another, depending on the value and the assessment they give to company’s purpose and motivation.

1.2 Stages of development of CSR

25into the corporate strategy

In recent years the sphere of Corporate Social Responsibility (CSR) has widened: it is therefore one of the dimensions of corporate strategy useful to survival and development. Large multi-business companies and their behavior influence and shape the markets, the society, the job, the ecological balance, and the relationships between Nations. It consists in practices such as sustainability, code of ethics, environmental certifications, but above all it aims to the satisfaction of social and economic expectations of stakeholders.

The forces that move the CSR can be grouped in economic macro-phenomena (for example globalization, sustainable development, human rights, responsible consumption, projects of corporate welfare), regulations, certifications, civil society, firms and much more. In its stages of development, CSR can have different configurations: informal, current, systematic,

25

Collis, D. J., & Montgomery, C. A., & Invernizzi, G., & Molteni, M., (January 2012), “Corporate level strategy:

15

innovative, dominant; along each of these stages, it increases the degree of integration of CSR into corporate strategy (figure 3). Move from one step to another means that the summit is driven by several factors like inevitability of the CSR, desire for concreteness, demand of competitive advantage, ideal tension.

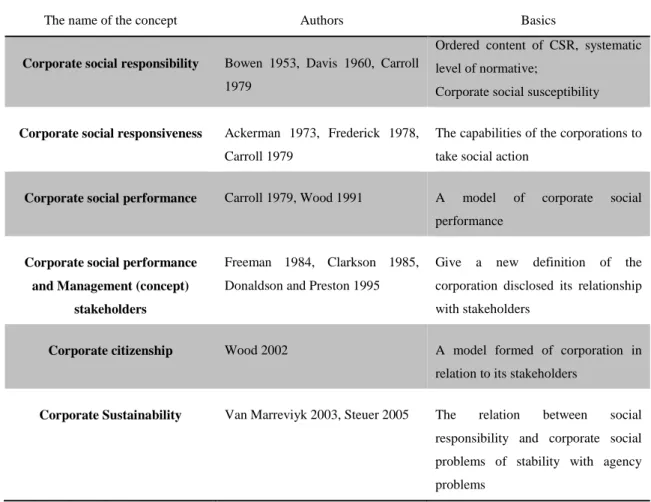

Table 1.1: the genesis of the concept of CSR.

The name of the concept Authors Basics

Corporate social responsibility Bowen 1953, Davis 1960, Carroll 1979

Ordered content of CSR, systematic level of normative;

Corporate social susceptibility

Corporate social responsiveness Ackerman 1973, Frederick 1978, Carroll 1979

The capabilities of the corporations to take social action

Corporate social performance Carroll 1979, Wood 1991 A model of corporate social performance

Corporate social performance and Management (concept)

stakeholders

Freeman 1984, Clarkson 1985, Donaldson and Preston 1995

Give a new definition of the corporation disclosed its relationship with stakeholders

Corporate citizenship Wood 2002 A model formed of corporation in relation to its stakeholders

Corporate Sustainability Van Marreviyk 2003, Steuer 2005 The relation between social responsibility and corporate social problems of stability with agency problems

Source: F.S. Madrakhimova, “Evolution of the Concept and Definition of Corporate Social Responsibility”, Global Conference on Business and Finance Proceedings, 2013, Vol. 8 NO.2

In the first stage, informal CSR, any initiative is evident or designed but surely each firm has experienced in its history measures for employees, environmental or social initiatives; in this way, management is aware of the phenomenon of CSR.

In the second stage, current CSR, the management implements classic practices like ethic code, sustainability account or marketing campaigns based on social causes; these practices should not be an attempt to imitate competitors but they should accompany firm in a process of transformation. The transition from current to systematic configuration is the most sensitive, because the change involves all the functions and all the business of the firm. To do well this step and to understand how to do, we could use the three methods named activity-based approach, stakeholder-based approach and benchmarking-based approach.

16

Figure 1.3: Stages of development of CSR into corporate strategy

Source: Collis, D. J., & Montgomey, C. A., & Invernizzi, G., & Molteni, M., (January 2012), “Corporate level strategy: generare valore condiviso nelle imprese multi

business”, 3a

Ed, pp. 397-446

1. The first is an approach based on the analysis of corporate activities through the model of the Value Chain by Porter: for each activity, the primary and the secondary, it’s good to involve all the managers in order to point out critics aspects of CSR in the activity and to identify the main stakeholder. As we know, primary activities are: inbound logistics, outbound logistics, operations, marketing and sales, services; secondary activities are: infrastructural activities, human resource management, technology development, procurement.

2. The second approach, compared with the previous, seeks to better understand the stakeholder’s expectations, making extensive use of listening and dialogue with them. Two theories are relevant: the stakeholder management and the stakeholder engagement. The first is based on seven point26: 1) managers should take into account interests of stakeholder in all decision-making processes; 2) managers should always talk about interests, contributes and risks; 3) manager should adopt procedures sensitive to stakeholder’s expectations; 4) fair distribution of costs and benefits resulting from business; 5) risks and damage should be minimized or compensated in appropriate way; 6) manager should avoid activity that should harm human rights; 7) manager should resolve conflicts about their role as stakeholder and as responsible of other stakeholder’s interests. The stakeholder engagement implies to take a stand on three aspects: what to talk about, who to involve, how to do. Usually stakeholders are

26

Clarkson Center for Business Ethics, (1999), “Principles of Stakeholder Management: the Clarkson Principles”, Toronto informal current systematic innovative dominant Level of integration into corporate strategy time Inevitability of CSR Desire of concreteness Competitive advantage Tension

17

selected on the basis of their power, the legitimacy and the urgency27; then, managers get a map of primary and secondary stakeholders and establish a dialogue with the first (they are usually shareholders, investors, employees, customers, suppliers, community). This dialogue may involve wide-ranging investigations, for example questionnaires about employees satisfaction, or consultations on specific topics, for example customer care on defective products. To achieve them, managers usually use meetings, like workshops or seminars, interviews, questionnaires, customer care through phone or website.

3. The benchmarking-based approach consists in the examination of existing policies throughout the business context, for example the best practices and forms of self-regulation, and it completes results of the two previous approaches. Finally, it could bring out efficient and profitable solutions for the firm.

Returning to the stages of CSR development, in the stage of innovative CSR the management combines social and business aspects configuring a “synthesis of socio-economic”, that can be analyzed depending on its growing impact on corporate strategy. So, following this order in an inverted pyramid there are functional initiatives at corporate level, strategic initiatives at corporate level, transversal projects, social and environmental business, profile of the corporate strategy.

Finally, in the CSR dominant, CSR is the earth of the vision and has a significant weight in decision-making processes.

Once the managers have found this set of possible solutions, they should compare them under two aspects: the social relevance (that of management, stakeholders and context) and the advantage for the firm (contrasting costs and benefits about actions of CSR)28. Just remember to be careful and update this studies, because these two aspects could change over time because of endogenous and exogenous factors.

Studying all these aspects and facing all issues, the managers could talk about creation of shared value.

1.3 Studies that converge into CSR

1.3.1 Stakeholder approaches to CSR

Stakeholders theory is one of the themes that converge as part of CSR. As we have already said, the first contribute in the literature on stakeholder theory came from Freeman in 1984 thanks to

27

Mitchell, R. K., & Agle, R. B., & Wood, D. J., (1997),“Toward a theory of Identification and Salience: Defining of

Principles of Who and What really Counts”, Academy of Management Review, Vol.22, pp. 853-886 28

Margolis, J. D., & Walsh, J. P., (2001),“People and Profits? The Search for a Link Between a Company’s Social

18

his Strategic Management: A Stakeholder Approach. The author defined stakeholders as “any group or individual who can affect or is affected by the achievement of the organization’s objectives” and in the same work he distinguished primary stakeholders from secondary stakeholders (figure 4), this distinction depending on the basis of the indispensability of their contribution to the survival of the firm. In fact, primary stakeholders are “all those individuals or group well identified from which the company depends for its survival: shareholders, employees, customers and governmental agencies”, so all the categories whose lack of contribution could decree the end of the company. Secondary stakeholders are “every clearly identifiable individual that may influence or may be influenced by organizations in terms of products, policies and business processes: […] groups of public interests, protest movements, local communities, institutions of government, business associations, labor unions and printers”, so their contributions could impact on reputation or profits but do not have relevant implication on the survival of the firm.

The purpose of stakeholder management was to devise methods to manage the myriad of groups and relationships that resulted in a strategic fashion; how we can see from Freeman’s definition of primary stakeholders, the company carrying out its functions it is required to respond to all stakeholders’ interests, and not only to the category that bring money, the shareholders, in order to better manage the business activity and to improve its development in the historical-social context. In fact, has we have already said, corporate performance was affected not only by firm’s shareholders but also by its stakeholders such as employees, customers and governments. And what are these interests? For sure they differ from one category to another: to make more money than those that invest, to receive satisfaction from work, to improve the reputation, to increase the confidence and to facilitate working relationship. But looking generally to the work of Freeman, we could say that:

it shows an attempt to make a fair balance or trade-off between economic and social purposes, including those of managers of a company and those of different stakeholders29: it’s not simply because it could be very difficult to identify all the interests or to distinguish acceptable and not acceptable demands; the theory does not show a mechanism to prioritize goals of the firm;

it does not take into account the sphere of moral values, identifying the work rather as a management strategy that defines the maximization of profits for the company and its stakeholders; about stakeholders theory, it is required to specify always which version refers (descriptive, instrumental, normative)30;

29

Donaldson, T., & Dunfee, T. W. (1999), “Ties that Bind: a Social Contracts Approach to Business Ethics:

Integrative social Contracts Theory”, Harvard Business School Press, Boston 30

Donaldson, T. & Preston, L.E. (1995), “The Stakeholder Theory of the Corporation: Concepts, Evidence and

19

the author does not make a clear distinction between those who should actually be considered a stakeholder and those who do not have the requirements to fall into this category that becomes, consequently, too wide and empirically non-functional31.

After Freeman’s work a lot of researches have tried to better explain the concept of stakeholders: Mitchell et al. in 1997 proposed a dynamic model that reaffirmed the importance of the perception of the organization from the management in order to define the map and the hierarchy of groups or individual with who it is necessary to liaise32. Then, Jahawar and McLaughlin33 wrote that the relationship between organization and stakeholders could change during the time through four steps (start up, emerging growth, maturity, decline or revival) and in which one would expect the position of the organization among stakeholders (reactive, defensive, negotiating, proactive). But also this model was considered too much rigid.

Figure 1.4: distinction between primary and secondary stakeholders

Source: comindwork.com; Comindwork weekly 1 April 2013 “Primary and secondary stakeholders of organization”;

Figure 1.5: distinction between internal and external stakeholders

Source: wikispaces.com

31

Andriof, J., & Waddock, S., & Husted, B., & and Rahman, S. (2002), “Unfolding Stakeholder thinking: Theory

Responsibility and Engagement”, 2 vol, Greenleaf, Sheffield 32

Mitchell, R. K., & Agle, B. R., & e Wood, D.J. (1997), “Toward A Theory of Stakeholder Identification and

Salience: Defining the Principle of How and What Really Counts”, Academy of Management Review, 22(4),

853-886

33

McLaughlin, G. L., & Jawahar, I. M., (2001), “Toward a descriptive stakeholder theory: an organizational life

20

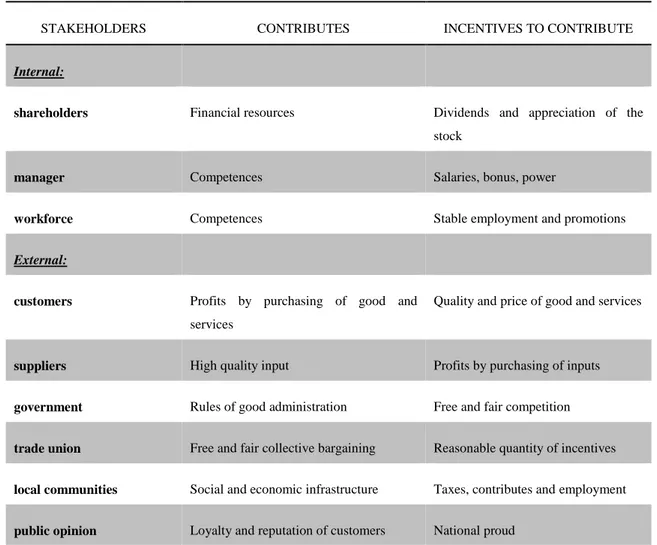

Table 1.2: internal and external stakeholders, contributes and incentives;

STAKEHOLDERS CONTRIBUTES INCENTIVES TO CONTRIBUTE

Internal:

shareholders Financial resources Dividends and appreciation of the stock

manager Competences Salaries, bonus, power

workforce Competences Stable employment and promotions

External:

customers Profits by purchasing of good and services

Quality and price of good and services

suppliers High quality input Profits by purchasing of inputs

government Rules of good administration Free and fair competition

trade union Free and fair collective bargaining Reasonable quantity of incentives

local communities Social and economic infrastructure Taxes, contributes and employment

public opinion Loyalty and reputation of customers National proud Source: Gareth Jones “Organizzazione: teoria, progettazione e cambiamento”, Egea, p. 26

Stakeholders could also classified as “internal” or “external” (figure 5) on the basis of contributions and incentives: companies exist because they have the ability to create value and to deliver convenient results for stakeholders. The latter are required to contribute to organization’s results if they expect higher incentives than contributions that are required to provide; contributes are considered competences and expertise that the firm requires to its members carrying out their tasks, while incentives are rewards such as money, power or organizational status. Internal stakeholders have interests on the resources of the firm (shareholders, manager and workforce), while external stakeholders do not participate in company’s ownership and do not depend from it but they have evenly interests (customers, suppliers, government, trade unions, local communities and public opinion). In table 2 are indicated the characteristics of the two categories.

For sure interests of stakeholders are different and goals of the company could satisfy one category more than others: sometimes firms prefer to satisfy economic interests and to realize profits maximization, but, even when a firm seeks to serve its shareholders as a primary

21

concern, its success in doing so is likely to be affected by all other stakeholders34. Some even argue that an inclusive stakeholder approach makes commercial sense, allowing the firm to maximize shareholder wealth, while also increasing total value added35. Then, the choice of goals is a very delicate phase for the company, in which it is good to consider and compare benefits and risks of each action.

Therefore, in the following work we will concentrate on the employees point of view and interests, in order to better understand the link between the actual practices of Corporate Social Responsibility of the firm to the employees’ work and also employees’ contribution to the value of the firm and to its competitive advantage. We will also underline the relevance of the human capital and the resource based view of the firm.

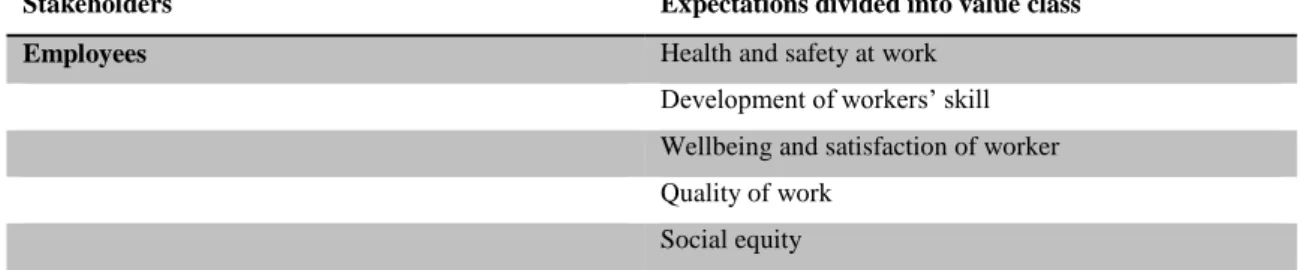

In the context of a sample Italian SMEs, Longo et al. (2005)36 identified the demand of key stakeholders regarding the creation of value by business, resulting in a grid of values (Table 3), where each stakeholder is associated with value classes that satisfied their respective expectations. Companies in their study are considered as socially responsible if they demonstrate social behavior satisfying the expectations of at least half of the value classes identified for each stakeholder (we will report only employees’ category). A similar approach was used by Abreu et al. (2005)37 that identified five key stakeholders related to CSR experience and practice of enterprises in Portugal and they examined workplace practices vis-à-vis employees; the results suggest the inclination of part of the firms to attend to the external dimension of CSR. In the context of Cypriot businesses, Papasolomou et al. (2005)38 used the stakeholder approach to identified six groups as a key stakeholders and to delineate relevant CSR actions vis-à-vis each cluster respectively (we will report only employees’ category) as we can see in Table 4. Their findings suggest that firms accord most attention to employees and customers in their pursuit of CSR, moderate attention to community stakeholder and limited attention to suppliers, investors and environment. Finally, one more case comes from Spain, where Uhlaner et al. (2004)39 define CSR effectiveness as the ability to satisfy a wide range of constituents within/outside organization; they identified two categories of stakeholders,

34

Foster, D., & Jonker, J., (2005), “Stakeholder Relationships: the Dialogue of Engagement”, Corporate Governance: The international journal of business in society, Vol. 5, Issue 5, pp. 51-57

35

Hawkins, D. E., (2006), “Corporate Social Responsibility: Balancing Tomorrow’s Sustainability And Today’s

Profits”, Palgrave McMillan, New York, pp. 142-150 36

Longo, M., & Mura, M., & Bonoli, A., (2005), “Corporate Social Responsibility and Corporate Performance: the

Case of Italian SMEs”, Corporate Governance: the international journal of business in society, Vol. 5, NO. 4, pp.

28-42

37 Abreu, R., & David, F., & Crowther, D., (2005), “Corporate Social Responsibility in Portugal: Empirical Evidence of Corporate Behaviour”, Corporate Governance: the international journal of business in society, Vol. 5,

Issue 5, pp. 3-18

38

Papasolomou-Doukakis, I., & Krambia-Kapardis, M., & Katsioloudes, M., (2005), “Corporate Social

Responsibility: the day forward? May be not!”, European Business Review, Vol. 17, Issue 3, pp. 263-279 39

Uhlaner, L. M., & van Goor-Balk, H. J. M., & Masurel, E., (2004), “Family Business and Corporate Social

Responsibility in a sample of Dutch Firms”, Journal of Small Business and Enterprise Development, Vol. 11, Issue 2,

22

economic and social, and findings suggest the salience of the economic stakeholders-customers and employees-over the social ones including sports club, the church and the environment. All the researches confirm on the basis of their study the utility of a stakeholder approach in the context of CSR.

Table 1.3: The grid of values

Stakeholders Expectations divided into value class Employees Health and safety at work

Development of workers’ skill Wellbeing and satisfaction of worker Quality of work

Social equity

Source: Longo, M., & Mura, M., & Bonoli, A., (2005), “Corporate Social Responsibility and Corporate

Performance: the Case of Italian SMEs”, Corporate Governance: the international journal of business in society, Vol.

5, NO. 4, pp. 28-42

Table 1.4: CSR actions vis-à-vis key stakeholders

Stakeholders Action vis-à-vis key stakeholders

Employees Provides a family friendly work environment Engages in responsible human resource management Provides an equitable reward and wage system for employees

Engages in open and flexible communications with employees

Invest in employee development

Encourages freedom of speech and promotes employee rights to speak up and report their concerns at work Provides child care support/paternity/maternity leave in addition to what it is expected by law

Engages in employment diversity in hiring and promoting women, ethnic minorities and the physically handicapped Promotes a dignified and fair treatment of all employees Source: Papasolomou-Doukakis, I., & Krambia-Kapardis, M., & Katsioloudes, M., (2005), “Corporate Social

Responsibility: the day forward? May be not!”, European Business Review, Vol. 17, Issue 3, pp. 263-279

1.3.2 Studies on Business Ethics

Another theme that converges as a part of CSR is the business ethic. These studies born in USA between 70s and 80s and concern the analysis of the goals that a company arises, of the rules that guide its conduct and, finally, of the principles and of the values that are the basis of its choices. As CSR, also business ethics cannot be defined exactly or uniquely because people have different standards of what is ethical or moral; but the minimum ethical standards could be honest business, observance of the law, compensation and job security for employees, hiring

23

practices40. The instrumental view of ethics shows as a firm can combine the highest ethical standards and operations economically rational, serving both shareholders and stakeholders41; in fact being unethical is very costly to the firm. For example, a firm that treats employees unethically may cause high turnover, expensive training, lower productivity, unethical behavior from the employees and, finally, higher costs of monitoring employees.

In the evolution of CSR and its definition, there is the lack of moral dimension which then is introduced by Frederick in order to emphasize the importance of ethical values acquired in regulating and governing the conduct of organization42. Epstein proposed a multidimensional definition of social responsibility, “corporate social policy process”, that included corporate social responsibility focused on effects of the firm into social context, corporate social responsiveness dedicated to definition of internal processes based on stakeholders’ interests, and business ethics based on moral values on which to base corporate policies43.

A lot of Italians researchers also contributed to the development of this theme. Sacconi defined the business ethics as “the study of the set of principles, values and ethical standards that govern (or should govern) various economic activities”, considering it as “applied ethic” to institution and economic practices conceived in different levels of abstraction: micro, meso and macro. In macro level, ethic is applied to moral valuation of principal economic institutions; in meso level, it’s applied to organizations and firms; in micro level, the moral evaluation is focused on managers’ choices44

.

Linked to CSR are also utilitarian theory and deontological theory: in the first one a strategic vision of CSR is supported, in the second one an ethic vision. According to the utilitarian theory, desires of people can be measureable as utility that minimizing problems maximizes pleasure; into an organization these moral choices could bring in the long run maximization of profit. But according to deontological theory there is a moral conscience intended as an absolute duty that must be respected; the duty of an organization is to subordinate its economic interests to the ethical principles, although this may lead to a reduction in profits.

Finally, it’s important to remember the government intervention in response to the increasing litigation concerning corporations accused of unethical behavior: in 1991 in the USA Federal Government passed the Sentencing Guidelines for Organizations (FSGO). It describes how an organization can be convicted of and punished for criminal conduct: the objective is to encourage ethical behavior by forcing all organizations to create ethics standards, convey them

40

Pitts, Kamery, (2002), “The role of business ethics”, Proceeding of the Academy of Legal, Ethical and Regulatory Issues, Vol. 6 NO 2.

41

Kotter, J. P., & Heskett, J. L., (1992), “Corporate culture and performance”, Free Press, New York, pp. 3-68

42

Frederick, W.C. (1986), “Toward CSR3: why ethical analysis in indispensable and unavoidable in corporate

affairs”, California Management Review, n.28, pp. 126-141 43

Epstein, E. M. (1987), “The corporate social policy process: beyond business ethics, corporate social

responsibility and corporate social responsiveness”, California Management Review, 29 (3), pp. 99-114 44

Sacconi, L. (1991), “Etica degli affari”, il Saggiatore, Milano; Sacconi, L. (2005), “Guida critica alla

24

to employees, monitor employees, and deal with employees who have violated their corporate ethics standards45. Corporations that implement effective compliance programs are less likely to be involved in criminal misconduct, to be subjects of criminal investigations, or to be prosecuted, and, if found guilty, may receive less onerous penalties and fines; so, compliance with the FSGO can lead to several positive outcomes that have direct benefits. The FSGO are used from corporations to: a) prevent and detect criminal conduct; b) reduce the risks associated with employee misconduct; c) minimize the likelihood of excessive penalties; d) protect their boards of directors from individual liability arising from noncompliant conduct. So, thanks to FSGO the business ethics programs are built around seven factors:

i. Establish compliance and procedures;

ii. Identify high-level personnel within the organization and assign overall responsibility; iii. Use due care in delegating discretionary authority;

iv. Effective communication with employees about training programs and practices; v. Use a reporting system whereby employees can report criminal conduct without fear of

retribution;

vi. Consistently enforce compliance standards through uniform disciplinary action;

vii. Take into account the possibility of changing programs in order to prevent violations of the law.

But, once an organization agrees to these points and with ethics activities, what should it do? The work proposed by Dubinsky shows ten steps that provide remarkably clear guidance: the steps describe what a company must do to create an ethics program that gives employees concrete direction and ensures consistency in decision-making.

Step 1: conduct a rigorous self-assessment (What do employees believe are our real values? What elements of an ethics and compliance program are already in place?); Step 2: ensure Commitment from the top of the organization (How does senior

management demonstrate their commitment and involvement? Are our leaders ethically neutral or ethically committed?);

Step 3: publish and distribute a Code of Ethics and related guidance materials (Do we have written guidance for all employees and stakeholders that explains our rules and expectations? Do the rules work for our business? Can employees find, read, and apply these rules?);

Step 4: communicate, communicate, and communicate once again (How are our messages communicated? Do employees hear and believe us? Are we effectively using electronic, visual and print media?);

45

25

Step 5: training (Do employees get timely training and learning opportunities that help them use the rules and values? How do we reinforce knowledge and use of our rules and values? Are we building a capacity among all employees to exercise moral judgment?);

Step 6: provide confidential resources (Where can employees go with problems, concerns, and allegations of misconduct? How reliable and trusted are those resources? Are confidences maintained? Can reports be made anonymously?);

Step 7: ensure consistent implementation (Do our systems work smoothly and efficiently? Are roles and responsibilities clear and well documented?);

Step 8: respond and enforce consistently, promptly and fairly (Are we consistent in applying our values, standards, and rules? Is discipline uniformly applied?);

Step 9: monitor and assess (What methods are used to evaluate our effort? Do employees receive feedback on our own internal scorecard?);

Step 10: revise and reform (Do we periodically update our values, rules and program content? Are we committed to continuous improvement?).

When all these standards are met, programs are sustainable over time.

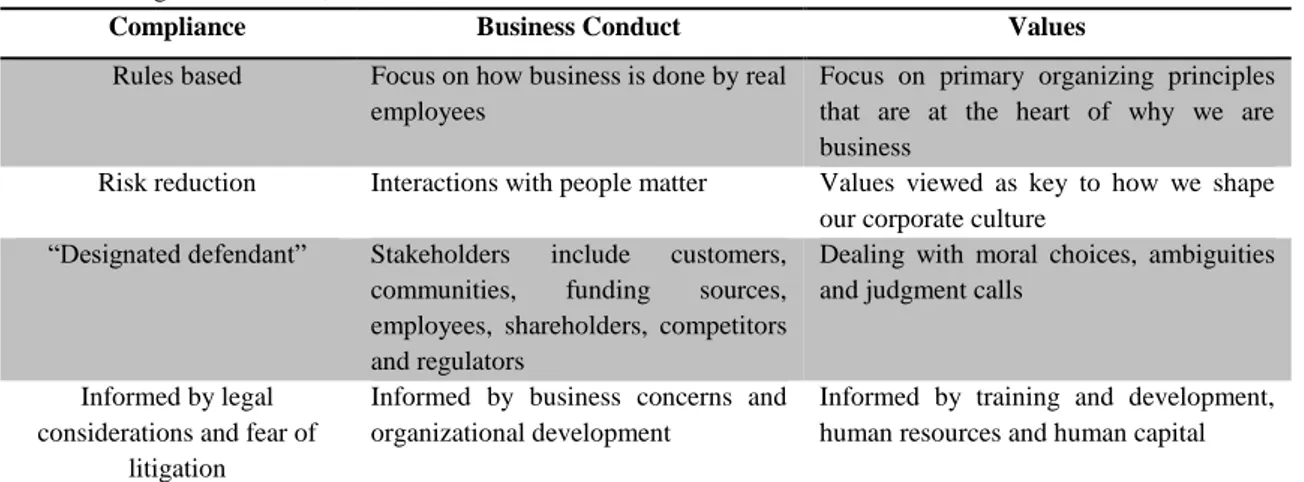

Finally, table 5 shows the evolution over the last 15 years of the underlying philosophies of corporate ethics programs.

Table 1.5: Program Evolution;

Compliance Business Conduct Values

Rules based Focus on how business is done by real employees

Focus on primary organizing principles that are at the heart of why we are business

Risk reduction Interactions with people matter Values viewed as key to how we shape our corporate culture

“Designated defendant” Stakeholders include customers, communities, funding sources, employees, shareholders, competitors and regulators

Dealing with moral choices, ambiguities and judgment calls

Informed by legal considerations and fear of

litigation

Informed by business concerns and organizational development

Informed by training and development, human resources and human capital Source: Dubinsky, A., (2002), “Business ethics: a set of practical tools”, Internal Auditing Magazine, Vol. 17 NO 4, pp. 39-45

1.4 Resource-based view of the firm and human capital

Now we will try to prove how the theory of the resource-based view (RBV) is linked with human capital, how the CSR could be a source of competitive advantage and how much employees are important from a strategic point of view.

26

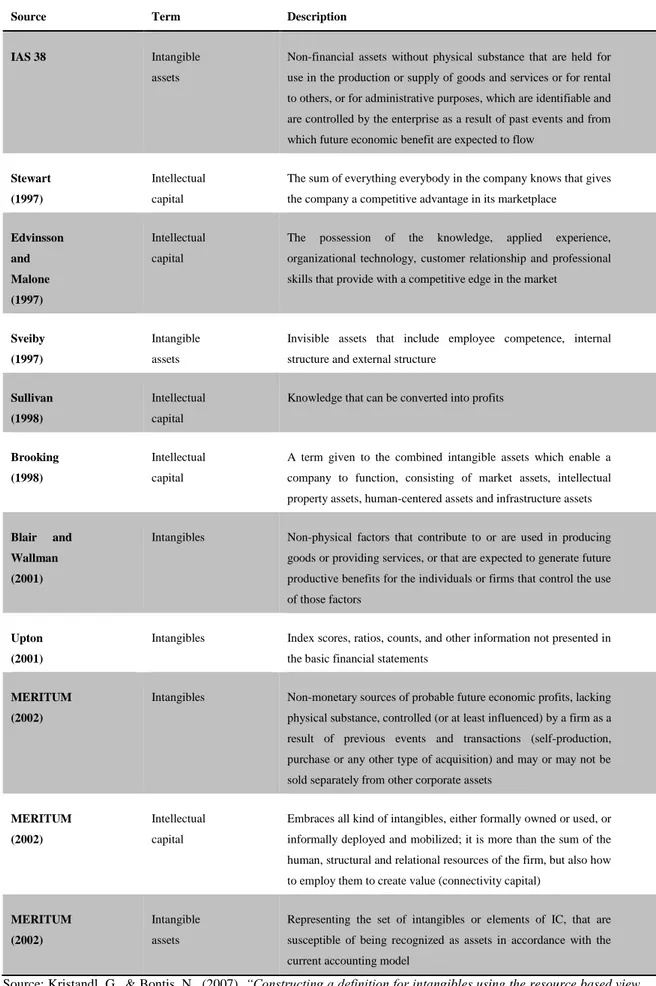

Table 1.6: selected definitions of intangibles;

Source Term Description

IAS 38 Intangible assets

Non-financial assets without physical substance that are held for use in the production or supply of goods and services or for rental to others, or for administrative purposes, which are identifiable and are controlled by the enterprise as a result of past events and from which future economic benefit are expected to flow

Stewart (1997)

Intellectual capital

The sum of everything everybody in the company knows that gives the company a competitive advantage in its marketplace

Edvinsson and Malone (1997) Intellectual capital

The possession of the knowledge, applied experience, organizational technology, customer relationship and professional skills that provide with a competitive edge in the market

Sveiby (1997)

Intangible assets

Invisible assets that include employee competence, internal structure and external structure

Sullivan (1998)

Intellectual capital

Knowledge that can be converted into profits

Brooking (1998)

Intellectual capital

A term given to the combined intangible assets which enable a company to function, consisting of market assets, intellectual property assets, human-centered assets and infrastructure assets

Blair and Wallman (2001)

Intangibles Non-physical factors that contribute to or are used in producing goods or providing services, or that are expected to generate future productive benefits for the individuals or firms that control the use of those factors

Upton (2001)

Intangibles Index scores, ratios, counts, and other information not presented in the basic financial statements

MERITUM (2002)

Intangibles Non-monetary sources of probable future economic profits, lacking physical substance, controlled (or at least influenced) by a firm as a result of previous events and transactions (self-production, purchase or any other type of acquisition) and may or may not be sold separately from other corporate assets

MERITUM (2002)

Intellectual capital

Embraces all kind of intangibles, either formally owned or used, or informally deployed and mobilized; it is more than the sum of the human, structural and relational resources of the firm, but also how to employ them to create value (connectivity capital)

MERITUM (2002)

Intangible assets

Representing the set of intangibles or elements of IC, that are susceptible of being recognized as assets in accordance with the current accounting model

Source: Kristandl, G., & Bontis, N., (2007), “Constructing a definition for intangibles using the resource based view